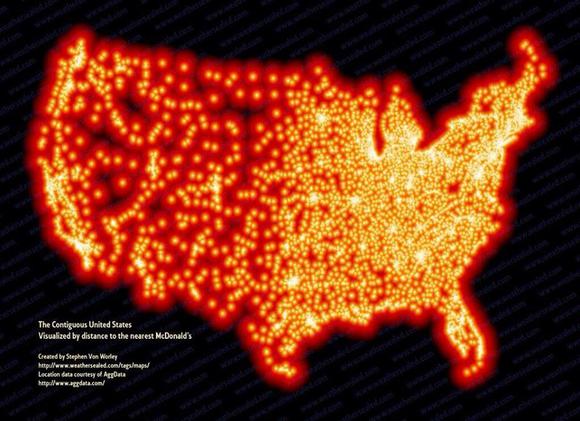

Can you imagine a world without McDonald’s Corporation (NYSE:MCD)? Well, at least we can all agree that there is no America without McDonald’s in the near future. The following graph is an amazing map of the United States visualized by distance to the nearest McDonald’s: the most clear depiction of McDonald’s Corporation (NYSE:MCD) leading market position. America, though, is not the exception; it is the rule. McDonald’s Corporation (NYSE:MCD) is the leading fast food chain in virtually every country where it operates, with the whole exception of China. Looking at the amazing scale the company has achieved, you might be wondering if there is further room available for growth in an increasingly fierce industry. I can bet my boots on that.

Illustration by Stephen Von Worley

Still growing

Can the world largest restaurant chain keep growing? Well, it’s happening. The latest earnings call showed a global comparable sales increase of 1.0% year over year and a consolidated revenues increase of 2%. Considering the enormous scale of operations that McDonald’s has achieved already (over 34,000 locations in more than 100 countries) and the not so easy environment (though pricing in the US and a 6.1% sales reduction in China for the second quarter, due to the negative impact from Avian Influenza), the numbers are quite respectable.

Therefore, not only is McDonald’s Corporation (NYSE:MCD) able to maintain its leading market position in most countries where it operates, but it is also growing its sales. A $700+ million marketing budget to keep the brand strong, free WiFi access and diversification of its coffee products is paying off. The above map showed us how far McDonald’s can penetrate a given economy and the success in America can, in theory, be replicated in other countries. Therefore, global expansion opportunities still exist for the biggest fast food chain.

Value stock

This shouldn’t be surprising, considering that McDonald’s Corporation (NYSE:MCD) has been able to consistently produced strong cash flow for the past 10 years. Owning 45% of the land and 70% of the buildings for its restaurants also brings more safety to the stock.

At the moment, McDonald’s shares remain rationally priced at 17 times earnings. The latest earnings call was not received well by investors (due to the short term negative outlook) and shares are trading at a significant discount from their all-time high of $103. Even better, most analysts and research firms agree with the fact that the latest earnings call negative outlook is not a strong reason enough to decrease their fair value estimates of McDonald’s. For example, Morningstar keeps a fair value estimate of $105 per share, almost $9 above the current price. Credit Suisse, on the other hand, has a $108 price target.

A simple dividend growth model also suggests McDonald’s Corporation (NYSE:MCD) may be a bargain. Assuming a 9% perpetual growth rate (which is reasonable considering that share buybacks will also help EPS to grow artificially) and that dividends will grow 9% annually for the next 10 years, suggests McDonalds fair value as a dividend stock would be $102 per share, also above the current trading price.

Amazing dividends

Dividends are another reason to fancy McDonald’s. McDonald’s has increased its dividend each of the past 35 years! Also keep in mind that the last 18 months saw a 26% jump. Since 2011 the company paid about $8 just in dividends. Therefore, investors who bought shares back then at $74 – $75 have benefited both from share price increases and dividends: an amazing overall 40% return on investment in 2 years. As McDonald’s continues increasing its dividends and the current stock price goes to the fair price estimate in the next months, I see a similar potential return for the next 2 years.

Graphic from “McDonald’s: A Deeper Look At Its 29% Dividend Growth Rate” article on Seeking Alpha

There may be many competitors in each country, but not even one strong competitor at a global scale

Let’s face it, there are plenty of competitors in each country. But there is not even one big global strong competitor. Perhaps some may think that Burger King Worldwide Inc (NYSE:BKW) is a strong global competitor, but unlike McDonald’s Corporation (NYSE:MCD), the company is losing sales. In the latest earnings call, it was reported that not only U.S. and Canadian comparable sales fell by 3% in the first quarter of the fiscal year, but the company is also experiencing trouble in Latin America, where sales fell another 1.3%. Notice that McDonald’s has far more resources than Burger King Worldwide Inc (NYSE:BKW) and this allows it to have negotiation power with its suppliers. For more information about the relation between Burger King and McDonald’s, check my short case for Burger King Worldwide Inc (NYSE:BKW).

The bottom line

There’s another reason for being long McDonald’s. Most fast food and restaurants are overvalued at the moment. Just to mention some examples Noodles & Co. is trading at a crazy 100x earnings and burrito shop Chipotle Mexican Grill, Inc. (NYSE:CMG) at a juicy 42 times multiple, well above the average valuation for a public company in the U.S. These 2 examples are growth stocks that became public recently.

But as growth stocks, there are plenty of risks in investing in them. For example, Noodles & Co. has forecasted 2,500 stores in the next 15-20 years. Although restaurant locations expanded by 15% since 2012 and sales grew by 17%, achieving 2500 stores means the company will have to keep its amazing growth rate for about 10 years, a very difficult challenge for any company to say the least.

Chipotle, on the other hand, had a tough 2012, as investors wonder if Chipotle Mexican Grill, Inc. (NYSE:CMG) can still grow or not. Also, unlike McDonald’s, Chipotle doesn’t have any negotiation power with its main suppliers due to its still small scale. That makes Chipotle vulnerable to minimum-wage increases, volatility in the price of beef, chicken and pork, and business cycles. If you own or are considering owning shares in Chipotle, you better check The Motley Fool’s special report now to get a deeper insight.

McDonald’s, on the other hand, isn’t a growth stock any more but it is a safe stock, as it has a long story of increasing dividends and a strong global brand. You know your grandchildren will eat McDonald’s Corporation (NYSE:MCD). Even better, it’s current PE ratio (17) is well below Noodles & Co. and Chipotle Mexican Grill, Inc. (NYSE:CMG). This could be a great time to go long the stock.

The article Why I’m lovin’ McDonald’s originally appeared on Fool.com and is written by Adrian Campos.

Adrian Campos has no position in any stocks mentioned. The Motley Fool recommends Burger King Worldwide, Chipotle Mexican Grill, and McDonald’s. The Motley Fool owns shares of Chipotle Mexican Grill and McDonald’s. Adrian is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.