Grocery stores have had a rough go of it since the recession, but one grocery store stands out from the pack and represents a great buy.

Industry Mechanics

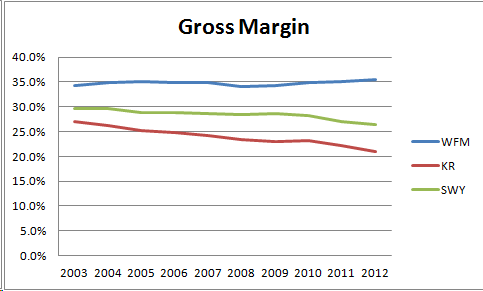

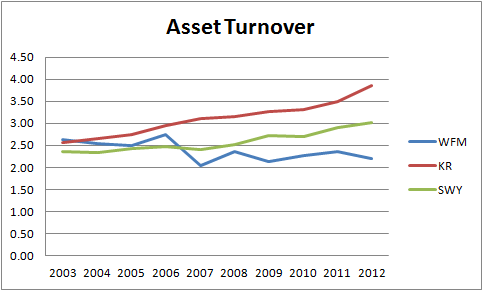

There are basically two ways to earn a profit in the grocery industry: earn a high margin or make a high number of sales per dollar of assets (asset turnover).

The most commonly-used model is based on asset turnover. Low prices and loss leaders are employed by the users of this model in an attempt to attract a loyal base of customers. These stores make up for low unit profitability by selling more units.

Organic grocers like Whole Foods Market, Inc. (NASDAQ:WFM) have had success charging high mark-ups on their products. While stores that earn high margins are not able to turn over their assets as quickly as those that compete on price, they earn a higher profit on each good sold. As a result, they are able to earn a respectable profit.

Three Case Studies

Whole Foods, Safeway Inc. (NYSE:SWY), and The Kroger Co. (NYSE:KR) each have their own styles in the grocery business. Whole Foods earns high margins, Safeway is a mix of high margin and high asset turnover, and Kroger has a high asset turnover.

Each strategy has different benefits and drawbacks, but only one of these companies is worth buying.

Whole Foods Market, Inc. (NASDAQ:WFM) is rare in that it still has substantial growth ahead of it in the United States. In addition, it will earn even higher profit margins as it expands its private-label offering.

Since 2002, Whole Foods has grown sales at an annualized rate of 15.7%. More impressively, it has grown pre-tax earnings at 17.8% per year over the same period. Its high growth rate is part of the reason why the company trades at a whopping 15x EV/EBITDA and 35x earnings.

But while Whole Foods’ business will continue to expand and improve over the next decade, the rich valuation will not reward investors. It’s best to stay away from Whole Foods for now.

While Whole Foods Market, Inc. (NASDAQ:WFM) earns high margins and a low asset turnover, Safeway sells only some of its products at a high margin and competes more on asset turnover. But the strategy has not been too successful.

Safeway began a re-branding effort in 2005 called ‘Lifestyle.’ Essentially, the company sells higher-margin products under its Lifestyle brand. However, margins have only decreased since the re-branding effort began.

On the plus side, the recent completion of Safeway’s re-branding efforts means that the company should earn more free cash flow in the future. Unfortunately, Safeway’s stores have not been able to recover customer traffic since the recession.

Safeway is in an awkward position between being a premium grocer that earns higher-than-discount margins and being a grocer that compete on price. The company will continue to decline until it picks a clear strategy.

However, Safeway is really cheap based on historical performance; it trades at just 4x EV/EBITDA and 10x earnings. It also trades at just 10x free cash flow even though free cash flow is expected to increase in the years ahead. But its recent performance makes the stock a pass.

Finally, The Kroger Co. (NYSE:KR) is a ‘premium’ store that has low prices where it counts and has a high asset turnover. The company has used its gas stations as a loss leader to drive customer traffic to its stores. This has allowed the company to gain market share while the rest of the industry backpedals from the recession. In addition, Kroger has a long runway for growth in the United States.

At just 4.3x EV/EBITDA and 15x normalized free cash flow, Kroger is not only a great company — it’s also inexpensive.

Best Bet in the Grocery Business

Whole Foods Market, Inc. (NASDAQ:WFM) is in the best position to take advantage of the long-term trend toward organic food, but its valuation is not attractive at all. Safeway is really cheap, but its future is uncertain and it will likely continue its decline for many years.

The Kroger Co. (NYSE:KR), on the other hand, has a solid base from which to expand and is currently being offered at a reasonable multiple of normalized free cash flow. A good business at a good price makes Kroger the best bet in the grocery business.

The article This Grocery Store Is the Best Bet originally appeared on Fool.com and is written by Ted Cooper.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.