Don’t get fooled by randomness

It’s important not to get caught up in the minute detail of looking at the banks. In truth they are still cyclical businesses. The banks make money when the economy is trading in the direction of the core assets (mortgages, loans, etc) on their loan book.

Therefore, if you want to buy banking stocks, you will need to focus on how the economy affects the quality of their loan books. If housing and the economy are doing well, then their credit quality (loan delinquencies, charge off rates) will get better, loan loss provisions will reduce, and demand for loans will go up. Ultimately higher rates should be a positive to their earnings in the long term. In turn, all of these metrics affect the valuation of the company.

My point here is that it’s the direction of the core assets, rather than looking at a snapshot of their earnings right now, that counts in terms of making a decision to buy the stocks.

The big question over the banks…

The key issue is how the banks might deal with a rising rate environment. The markets have been keen to price in higher rates ever since Ben Bernanke implied that the Federal Reserve would begin tapering bond-market purchases. So where does this leave the banks? Will rising rates choke off loan demand, or will the housing market continue to recover despite them? Naturally, if the latter occurs, the banks will see increased loan demand and banking profitability.

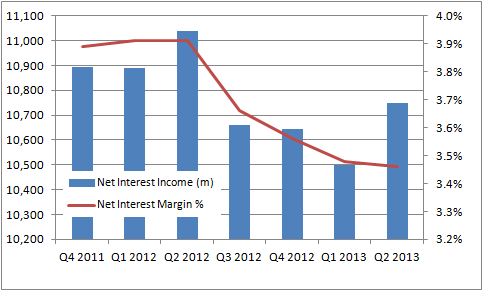

The issue can be seen by looking at Wells Fargo & Co (NYSE:WFC)’s net income and its net interest margin (NIM). Interest income (roughly half of income) is more important to follow than non-interest income, because it is more variable.

The market has been fretting over this issue in 2013 as economic growth (therefore loan demand growth) has been moderate, while interest rates remain low (reduced interest rate income) and deposit growth has grown strongly (consumers continuing to deleverage).

Meanwhile, financial services companies such as Capital One Financial Corp. (NYSE:COF) have been experiencing run-off. This is where existing loans are paid off and not replaced by new loans due to weak demand. Indeed, Capital One Financial Corp. (NYSE:COF) expects run-off to be $12 billion in 2013 and a further $8.5 billion in 2014.

Furthermore, JPMorgan Chase & Co. (NYSE:JPM)’s CEO, Jamie Dimon, discussed the possibility for a “dramatic reduction” in the bank’s mortgage profits if rising rates slowed demand for home loans. The issue is highly relevant because Wells Fargo & Co (NYSE:WFC) JPMorgan are the two biggest mortgage lenders in the U.S. Moreover, as the housing market is a key determinant for the ‘wealth effect’, the banks can expect demand for other forms of credit (auto loans, credit card, etc) to be indirectly tied to it.

The two reasons why the banks will do well

The first cause for optimism is that the increase in deposit growth created by consumer de-leveraging is building a powerful asset base from which the banks can lend. For example, here is how Wells Fargo & Co (NYSE:WFC)’s average core deposits have increased recently:

In addition, its tier 1 capital ratio (a common measure of a bank’s capital adequacy) has been rising. This indicates an increased capacity to lend.

The second reason is that the wealth effect from housing is real. Here is a graph of data from the Federal Reserve that demonstrates how U.S. households and nonprofit organizations have seen real restate wealth and their net worth improve in recent years:

Furthermore, gains in employment and slow-but-steady economic growth are creating a favorable environment for growth in loan demand. If these conditions persist, then the banks should be able to deal with a rising rate environment. Indeed, historically speaking, a rising rate environment means that banks will make more money.

The bottom line

In conclusion, investors should stay positive on the financial services sector as long as the underlying fundamentals are moving in a favorable direction. The debate about the effects of rising rates on the economy will go on and on. There will be tomes of spilled ink discussing the NIM, run-off, Basel III and other esoteric concepts that ordinary investors find hard to grasp.

However, Bernanke has made it clear that tapering the purchases of bonds –therefore lowering interest rates– is contingent upon a stronger economy. Either the Federal Reserve will try to lower rates in the future (given a slowing economy), or the economy will get better (implying more loan demand). In any case, the banks are being supported in their activities and, unless the economy is heading towards another recession, investors should look to hold some banking stocks in their portfolio.

The article Why You Should Stay Invested in the Financial Sector originally appeared on Fool.com and is written by Lee Samaha.

Lee Samaha has no position in any stocks mentioned. The Motley Fool recommends Wells Fargo & Co (NYSE:WFC). The Motley Fool owns shares of JPMorgan Chase & Co. (NYSE:JPM). and Wells Fargo. Lee is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.