While most dividend paying stocks that trade on exchanges in the US pay quarterly, there are some stocks that pay their dividends on other schedules.

A handful pay their dividends semi-annually while a there is a larger population of monthly dividend stocks. While only one aspect that should be considered in selecting stocks for investment, monthly dividend payments can be advantageous for building wealth over time and to smooth out a dividend retirement income stream.

In my own personal portfolio, the largest portion of my stock holdings make dividend payouts in May, August, November, and February. I have to manage the family finances to ensure those quarterly payments last until the next quarter’s payments. If the majority of my holdings were monthly dividend stocks, it would be easier to manage the family’s cash flow.

As I inferred above, I and my family live off our investment income so I do not use a Dividend Reinvestment Plan (DRIP). We spend most of the investment income our portfolio generates. However, when I was working hard to build wealth, I did use DRIPs often to insure I had a systematic and disciplined investment strategy. There is a small benefit to be gained through monthly compounding in a DRIP versus quarterly compounding. Monthly compounding grows wealth just a little bit faster than quarterly compounding. The chart below provides that comparison.

The chart above shows the annual growth of $1.00 invested in a stock paying a 6% dividend for 25 years. On this scale it is hard to see much of a difference until the period between 20 and 25 years where the red and blue lines diverge.

To get a complete understanding of the benefit of monthly compounding, if you had an initial investment of $10,000 and had reinvested a 6% quarterly dividend (quarterly compounding) you would have $59,693 after 30 years. If the stock was instead a monthly dividend paying stock with the dividend reinvested, you would have $60,226 after 30 years. Every little advantage available should be exploited, especially in today’s market.

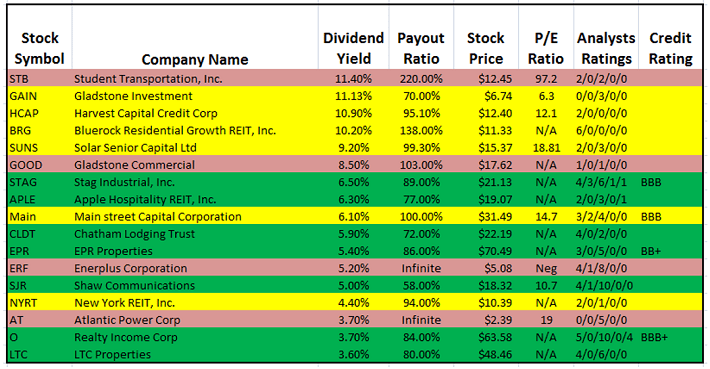

17 Monthly Dividend Stocks

You might be wondering why I chose 6% for the dividend rate when so few healthy companies are paying out dividends at that rate. The answer is that there are a number of companies out there that:

1. Pay dividends of 6% (plus or minus)

2. Are growing those dividends

3. Have solid balance sheets

A handful of these businesses even have investment grade credit ratings.

The table below provides a list of 17 monthly dividend stocks sorted on dividend yield.

It should be noted that this list is not all inclusive of monthly dividend paying stocks as there were a few monthly distribution paying master limited partnerships (MLPs) and a couple of crude oil production trusts that I chose to leave off this initial list of stocks.

MLPs and crude oil trusts are not stocks and their accounting and financial reporting is sufficiently different that they should be covered separately.

The “Analysts Ratings” column of the spreadsheet should be interpreted as Buy/Outperform/Hold/Underperform/Sell.

For example: STAG with 4/3/6/1/1 would be interpreted as 4 analysts rate STAG as a BUY, 3 analysts rate STAG as OUTPERFORM, 6 rate STAG as a HOLD, 1 analyst rates STAG as UNDERPERFORM, and 1 rates STAG as a SELL. I view analysts ratings as one indicator to consider when evaluating a stock for potential investment versus a definitive metric.

The colors in the chart do have meaning. The stocks highlighted in red are equities that I personally would not currently have in my portfolio. Those stocks highlighted in yellow are stocks that I would consider including in my portfolio under the right conditions and in moderation. Investors need to understand their own appetite for risk and invest accordingly. Those stocks that are listed in green are those stocks that I now have in my portfolio, previously had in my portfolio, or would do so in the future given acceptable valuation metrics.

Readers will note that the top half of the spreadsheet above has more red and yellow. High dividend yields also often indicate there might be fundamental issues with a company’s financials or business prospects and indeed the higher dividend stocks are also at the top of the spreadsheet.

That is not to say that a high dividend is a clear and unambiguous indicator of underlying financial problems but, it should cause an investor to pause and carefully evaluate before committing money.

Rather than rely only on red/yellow/green indicators, I’ve provided a short summary and investment thesis on each stock.

Student Transportation Inc (NASDAQ:STB)

Student Transportation Inc (NASDAQ:STB) provides school bus transportation services as well as investment in oil and gas interests. The Transportation segment provides school bus and management services to public and private schools in North America. The Oil & Gas segment represents the company’s investments as a non-operator in oil and gas production in the Canadian Provinces. The company was founded by Denis J. Gallagher on May 15, 1997 and is headquartered in Barrie, Canada.

There are a couple of factors that, for me, make STB not suitable for investment at this time. First and foremost is the difficulty STB has had covering its dividend. The current payout ratio is 220% and Student Transportation Inc (NASDAQ:STB) has not covered its dividend payment for the last few quarters. I expect a dividend cut is forthcoming.

The second negative indicator for me is the company attempting operate in two widely differing types of business; school bus transportation services and investments in oil and gas production. I’m not sure I could devise two more disparate businesses under the same roof.

STB was in the portfolios of just three of the investment firms tracked by Insider Monkey on December 31, with those money managers having ownership of just 0.70% of the company’s shares. Jim Simons’ quant fund Renaissance Technologies owned most of those, with a 663,100-share position valued at $2.46 million at the end of 2015.

Gladstone Investment Corporation (NASDAQ:GAIN)

Gladstone Investment Corporation (NASDAQ:GAIN), a business development company (BDC), invests in small and medium sized companies located in the US, with EBITDA of $3 million or more, positive cash flows, strong competitive position in an industry, liquidation value of assets sufficient to cover debt, and experienced management. It makes debt investments in the form of senior debt and senior/junior subordinated debt and equity investments in the form of common equity, preferred equity warrants for buyouts/change of control, acquisition, growth and recapitalization transactions. GAIN acquires controlling interests with an investment size ranging from $5 to $30 million. It also makes co-investments and may take a seat on the board of directors.

GAIN is covering its dividend, has a very reasonable P/E of 6.3, and has very attractive dividend at 11.1% yield. On the negative side, GAIN is externally managed by a company (Gladstone Management) that also manages several other entities and therefore may not be fully aligned with shareholder interests.

In addition Gladstone Investment Corporation (NASDAQ:GAIN) is a small cap company without a credit rating which results in its cost of capital being higher than some of its better established competitors. However, this BDC may be suitable for an investor that can tolerate a higher level of risk. The high dividend reflects the risk investors have in ownership of this equity.

Follow Gladstone Investment Corporation (NASDAQ:GAIN)

Follow Gladstone Investment Corporation (NASDAQ:GAIN)

Receive real-time insider trading and news alerts

Harvest Capital Credit Corp (NASDAQ:HCAP)

Harvest Capital Credit Corp (NASDAQ:HCAP) is a non-diversified management investment company which provides customized financing to small and midsized businesses. HCAP’s products include senior secured debt, uni-tranche term loans, junior secured term loans, subordinated debt investments and minority equity co-investments. The company was founded by Richard Paul Buckanavage on November 14, 2012 and is headquartered in New York, NY.

A small position in HCAP might be appropriate for the more risk tolerant investors. Because it is a relatively new small cap BDC, it is inherently a riskier investment. On the positive side, the P/E is a very reasonable 12.1, it is (barely) covering its dividend, and the two analysts that cover Harvest Capital Credit Corp (NASDAQ:HCAP) have rated it as a buy. The current 10.9% dividend yield is high and reflects the additional risk that investors have in owning shares in this stock.

Follow Harvest Capital Credit Corp (NASDAQ:HCAP)

Follow Harvest Capital Credit Corp (NASDAQ:HCAP)

Receive real-time insider trading and news alerts

Bluerock Residential Growth REIT Inc (NYSEMKT:BRG)

Bluerock Residential Growth REIT Inc (NYSEMKT:BRG) operates as a real estate investment trust. Its business is raising capital and acquiring a diverse portfolio of residential real estate assets. The company investment objective is to acquire and develop a diversified portfolio of real estate investments, with a focus on well-located, Class A apartment properties with strong and stable cash flows. The company was founded on July 25, 2008 and is headquartered in New York, NY.

BRG is another mixed bag. Since their founding in 2008, BRG has grown significantly and has achieved their goal of acquiring a diverse portfolio of class A properties. But it has a few negatives that keep me from taking a position in this REIT. It is externally managed which often makes it difficult for management to be fully aligned with the goals and objectives of the company and its share holders. I strongly prefer internal management.

Bluerock Residential Growth REIT Inc (NYSEMKT:BRG) is getting closer but has not yet been able to consistently cover their dividend which is a lofty 10.2% yield. Because it is small, it has no credit rating so its cost of capital is higher than its larger and better established competitors. The price-to-earnings ratio is not a meaningful metric for REIT evaluation so I have not listed it in the spreadsheet above. All that said, given the progress that BRG has made since 2008, it may be a candidate for the risk tolerant investor.

Follow Bluerock Residential Growth Reit Inc. (AMEX:BRG)

Follow Bluerock Residential Growth Reit Inc. (AMEX:BRG)

Receive real-time insider trading and news alerts

Solar Senior Capital Ltd (NASDAQ:SUNS)

Solar Senior Capital Ltd (NASDAQ:SUNS), as a BDC, invests in middle market companies across the globe, primarily in the US with companies having EBITDA in the range of $20 – $100 million. The fund targets companies operating in the fields of diversified financial services, communications equipment, insurance, health care services, software, food products, specialty retail, professional services, internet software and services, air freight and logistics distributors, IT services, automotive retail, healthcare technology, hotels, restaurants and leisure, containers and packaging, capital markets, footwear, aerospace and defense industrial conglomerates and diversified consumer services. It provides financing in the form of senior secured loans, mezzanine loans and equity securities with an investment size of $5 – $30 million.

Solar Senior Capital Ltd (NASDAQ:SUNS) is a small cap BDC just barely covering their 9.3% yield dividend. Their P/E is on the high side at 18.8. Shares of SUNS might be suitable for investors with a higher risk tolerance but it is not a sleep well at night (SWAN) investment in that it should be closely monitored for any signs of financial stress.

Follow Slr Senior Investment Corp. (NASDAQ:SUNS)

Follow Slr Senior Investment Corp. (NASDAQ:SUNS)

Receive real-time insider trading and news alerts

Gladstone Commercial Corporation (NASDAQ:GOOD)

Gladstone Commercial Corporation (NASDAQ:GOOD) is an externally managed real estate investment trust that invests in and owns net leased industrial, commercial and retail property and selectively makes long-term industrial and commercial mortgage loans. Its portfolio consists primarily of single-tenant commercial and industrial real property. The company also owns multi-tenant commercial and industrial properties, as well as retail and medical properties. Its portfolio of real estate is leased to a wide cross section of tenants ranging from small businesses to large public companies, many of which are corporations that do not have publicly rated debt. Gladstone Commercial was founded by David John Gladstone on February 14, 2003 and is headquartered in McLean, VA.

Gladstone Commercial Corporation (NASDAQ:GOOD) is a small cap triple net lease REIT that also makes some commercial loans. As I noted above, P/E is not a meaningful metric for REIT evaluation. GOOD is not currently covering their dividend payout with the dividend/FFO (funds from operations) ratio at 103%. In addition, the REIT is externally managed which often results in management not being fully aligned with share holders. I would not consider GOOD for my own portfolio for these reasons.

Follow Gladstone Commercial Corp (NASDAQ:GOOD)

Follow Gladstone Commercial Corp (NASDAQ:GOOD)

Receive real-time insider trading and news alerts

Stag Industrial Inc (NYSE:STAG)

Stag Industrial Inc (NYSE:STAG) is a real estate investment trust, which focuses on the acquisition and operation of single-tenant, industrial properties throughout the United States. It endeavors to identify relative value investments across all locations, industries and tenants among these properties through the application of a company proprietary risk assessment model, operate those properties in a profitable manner, and capitalize business appropriately given the characteristics of assets. The company was founded on July 21, 2010 and is headquartered in Boston, MA.

Stag Industrial Inc (NYSE:STAG) is one of my larger holdings, pays a healthy dividend of 6.5% with a FFO payout ratio of 89%. STAG is covered by 15 analysts with generally favorable ratings on the stock. Significantly, STAG maintains a BBB investment grade credit rating which provides them access to capital markets at favorable rates. I initiated my investment in STAG almost 2 years ago after fairly extensive due diligence on the company and its operations. STAG 1Q16 financials came in strong and the market has begun to take notice of STAGs performance and potential.

Follow Stag Industrial Inc. (NYSE:STAG)

Follow Stag Industrial Inc. (NYSE:STAG)

Receive real-time insider trading and news alerts

Apple Hospitality REIT Inc (NYSE:APLE)

Apple Hospitality REIT Inc (NYSE:APLE), invests in income-producing real estate, primarily in the lodging sector, in the United States. Its hotels operate under Marriott or Hilton brands. The company has wholly-owned taxable REIT subsidiaries, which lease all of the company’s hotels from wholly-owned qualified REIT subsidiaries. Apple Hospitality REIT was founded in November 2007, went public in 2015, and is headquartered in Richmond, VA.

Apple Hospitality REIT Inc (NYSE:APLE) is a relative new comer with respect to having gone public in 2015 though it is a large cap REIT having been operated privately since 2007. It is a little too new for me to add to my portfolio but I do have it on my watch list. APLE recently reported 1Q16 financial performance and the company beat analyst’s projections on both the top and bottom line. Payout ratio is a healthy 77% and analysts ratings are generally favorable. I listed this stock in the spreadsheet as green because the only thing holding me back from an investment now is that I’d like to see another couple quarters of financials before I commit. For the interested reader, more detail can be found on APLE here and here.

Follow Apple Hospitality Reit Inc. (NYSE:APLE)

Follow Apple Hospitality Reit Inc. (NYSE:APLE)

Receive real-time insider trading and news alerts

Main Street Capital Corporation (NYSE:MAIN)

Main Street Capital Corporation (NYSE:MAIN) a BDC that invests in lower middle market companies with revenues of $10 – $150 million and EBITDA of $3 – $20 million. The fund targets companies operating in the fields of communications, electronic technology, finance, commercial services, restaurants, health services, consumer services, producer manufacturing, technology services and non energy minerals. It provides debt, equity and warrant financing for growth, management buyouts, recapitalizations, refinancing and acquisitions.

Main Street Capital Corporation (NYSE:MAIN) is a large cap BDC with a reasonable P/E of 14.7 and carries a BBB credit rating. The nine analysts that cover MAIN have generally favorable ratings on the company. The negative with MAIN is the razor thin coverage of the current dividend at a 100% payout ratio. While the market will often forgive a company for not fully covering a dividend in one or two quarters, the market can also be brutal on companies that cannot cover dividend payments for more than a couple quarters. I try very hard to maintain my capital base and so have listed MAIN as yellow; suitable for more risk tolerant investors. For the interested reader, I previously published an article on the importance of maintaining investment capital.

Follow Main Street Capital Corp (NYSE:MAIN)

Follow Main Street Capital Corp (NYSE:MAIN)

Receive real-time insider trading and news alerts

Chatham Lodging Trust (NYSE:CLDT)

Chatham Lodging Trust (NYSE:CLDT) operates as a real estate investment trust organized to invest in upscale extended-stay hotels. It includes investing in premium-branded select-service hotels such as Courtyard by Marriott, Hampton Inn and Hampton Inn and Suites. The company was founded on October 26, 2009 and is headquartered in West Palm Beach, FL.

Chatham Lodging Trust (NYSE:CLDT) is a mid cap sized REIT that is growing quickly. It offers a 5.9% dividend yield with a very comfortable FFO payout ratio of 72%. The analysts that cover CLDT have generally favorable ratings on the trust. CLDT recently reported 1Q16 financial performance that met or beat analyst’s expectations. The only thing CLDT really lacks is a credit rating though the company does maintain a solid balance sheet. With a little more time and size, I’m sure CLDT will pursue a formal credit rating from the major rating agencies. I’ve listed CLDT as green in the spreadsheet based on their overall performance to date. While I don’t own shares of CLDT in my portfolio, I do carry it on my watch list.

Follow Chatham Lodging Trust (NYSE:CLDT)

Follow Chatham Lodging Trust (NYSE:CLDT)

Receive real-time insider trading and news alerts

EPR Properties (NYSE:EPR)

EPR Properties (NYSE:EPR) is a real estate investment trust. It engages in the development, finance, and leasing of theatres, entertainment retail and family entertainment centers. EPR operates in the following segments: Entertainment, Education, Recreation, and Other. The Entertainment segment consisted of investments in large megaplex theatres, entertainment retail centers, family entertainment centers and other retail parcels. The Education segment consists entirely of investments in public charter schools. The Recreation segment consists of investments in metro ski parks, water-parks and golf entertainment complexes. The Other segment consists of investments in vineyards and wineries and land held for development. The company was founded by Peter C. Brown on August 29, 1997 and is headquartered in Kansas City, MO.

EPR Properties (NYSE:EPR) is a large cap REIT that covers a lot of different types of real estate investment. It offers a respectable 5.4% dividend with a FFO coverage ratio of 86%. The eight analysts covering EPR give it generally favorable ratings. The one negative on EPR is the BB+ credit rating which is less than investment grade. I do have EPR on my watch list but I don’t currently have a position in the stock. I have listed the stock green based on its fundamentals and its performance to date.

Follow Epr Properties (NYSE:EPR)

Follow Epr Properties (NYSE:EPR)

Receive real-time insider trading and news alerts

Enerplus Corp (USA) (NYSE:ERF)

Enerplus Corp (USA) (NYSE:ERF) engages in the exploration and production of oil and gas. The company’s oil and gas assets are located in Willston Basin, Macellus, Waterfoolds, and Deep Basin. Enerplus was founded in 1986 and is headquartered in Calgary, Canada

Enerplus Corp (USA) (NYSE:ERF) is an oil and gas E&P company. Like most other companies in the sector, ERF has been hammered by the market depressing the share price and raising the dividend yield. The company is not able to cover the dividend payment and currently has negative earnings. Until the oil and gas market prices firm up, ERF will continue to suffer. This stock is suitable only for investors comfortable with speculative investments.

Follow Enerplus Resources Fund (NYSE:ERF)

Follow Enerplus Resources Fund (NYSE:ERF)

Receive real-time insider trading and news alerts

Shaw Communications Inc (USA) (NYSE:SJR)

Shaw Communications Inc (USA) (NYSE:SJR) operates as a diversified communications and media company, providing consumers with broadband cable television, Internet, home phone, telecommunications services, satellite direct-to-home services and engaging programming content. SJR operates through three segments: Cable, Satellite and Media. The Cable segment includes cable television, Internet, digital phone and Shaw business operations. The Satellite segment comprises of direct-to-home and satellite services. The Media segment engages in the business of television broadcasting. The company was founded by James Robert Shaw on December 9, 1966 and is headquartered in Calgary, Canada.

Shaw Communications Inc (USA) (NYSE:SJR) is a large cap telecommunications company but is the smallest of the four major telecom companies in Canada. The company currently offers a 5% dividend with a very comfortable 58% payout ratio and a P/E of 10.7. The company is planning for significant growth in its Canadian operations. Analysts’ ratings of SJR are generally favorable. I don’t currently own SJR but I do have it on my watch list. Investors should note that currently the Canadian loonie is weak compared to the US dollar due to Canada’s economy. When Canada’s economy picks up (e.g. when crude oil prices recover), the loonie will also strengthen and the value of investments in Canadian companies will rise as will the US dollar value of their dividends.

Follow Shaw Communications Inc (NYSE:SJR)

Follow Shaw Communications Inc (NYSE:SJR)

Receive real-time insider trading and news alerts

New York REIT Inc (NYSE:NYRT)

New York REIT Inc (NYSE:NYRT) is a real estate investment trust which acquires income-producing commercial real estate including office and retail properties in New York. The company was formerly known as American Realty Capital New York Recovery REIT, Inc. New York REIT was founded on October 6, 2009 and is headquartered in New York, NY.

New York REIT Inc (NYSE:NYRT) is a mid cap equity REIT with a portfolio of class A properties. It is a relatively new REIT and, as such, does not yet have a credit rating. It offers a 4% dividend yield and favorable analyst ratings but its FFO dividend payout ratio is pretty thin at 94%. This REIT is more suited to risk tolerant investors and I would add that I don’t believe the current dividend offers sufficient compensation for the additional risk of owning this new unrated REIT. A recent article published on Seeking Alpha makes the case for NYRT’s valuation based on the quality of the properties in its portfolio. For those interested in following up on NYRT, the article can be found here.

Follow New York Reit Inc. (NYSE:NYRT)

Follow New York Reit Inc. (NYSE:NYRT)

Receive real-time insider trading and news alerts

Atlantic Power Corp (NYSE:AT)

Atlantic Power Corp (NYSE:AT) is a monthly dividend stock that owns and operates a fleet of power generation assets in the United States and Canada. Its power generation projects sell electricity to utilities and other large commercial customers under long-term power purchase agreement. It operates through the following segments: East U.S., West U.S., Canada, and Un-Allocated Corporate. The company was founded on June 18, 2004 and is headquartered in Dedham, MA.

Atlantic Power Corp (NYSE:AT) has fallen on hard times. As a merchant fleet operator (unregulated), it sells electricity at market rates. Electricity rates have fallen across the country recently mainly because the price of natural gas has been hovering around $2/MBtu for the last couple of years. AT’s current share price reflects a company under stress and not one I would invest in at this time.

Follow Atlantic Power Corp (NYSE:AT)

Follow Atlantic Power Corp (NYSE:AT)

Receive real-time insider trading and news alerts

Realty Income Corp (NYSE:O)

Realty Income Corp (NYSE:O) is a real estate company with the primary business objective of generating dependable monthly cash dividends from a consistent and predictable level of cash flow from operations. Realty Income was founded by William E. Clark, Jr. and Evelyn Joan Clark in 1969 and is headquartered in San Diego, CA.

Realty Income Corp (NYSE:O) is one of the oldest REITs and one of the most successful; so successful that it has almost a cult following. Like all the stocks highlighted in this article, Realty Income is a monthly dividend stock. In addition, it is known for raising that dividend at least every quarter. The success of the this REIT has resulted in the share price being pushed up to the point where I sold out my holdings. I did not sell because Realty Income’s performance has dropped but because I had a 38% gain in the stock and could reinvest the proceeds for a higher return. When the market comes to its senses again and Realty Income’s valuation is fair again, I’ll reinvest in the company. But at a yield of 3.6%, Realty Income is overvalued. The company has a solid balance sheet and carries a BBB+ credit rating; one of the highest in the REIT sector. I’ve listed the company as green in the spreadsheet but recommend that investors wait until a more favorable valuation is offered for Realty Income.

Follow Realty Income Corp (NYSE:O)

Follow Realty Income Corp (NYSE:O)

Receive real-time insider trading and news alerts

LTC Properties Inc (NYSE:LTC)

LTC Properties Inc (NYSE:LTC) operates as an internally managed REIT that invests primarily in the long-term care sector of the health care industry through the origination of first mortgage loans and acquisition of properties that are leased to long-term care providers. Its primary senior housing and long term healthcare property types include Skilled Nursing, Assisted Living Properties and Independent Living Properties. LTC Properties was founded by Andre C. Dimitriadis on May 12, 1992 and is headquartered in Westlake Village, CA.

LTC Properties Inc (NYSE:LTC) is a mid cap REIT with a history of conservative growth. Though is does not have a credit rating from any of the rating agencies due to its size, LTC has a solid balance sheet and a reasonable dividend payout ratio of 80% of FFO. This is another very solid REIT but, like Realty Income, suffers currently from over valuation. I recommend that investors wait for a lower valuation to invest in LTC.

Follow Ltc Properties Inc (NYSE:LTC)

Follow Ltc Properties Inc (NYSE:LTC)

Receive real-time insider trading and news alerts

Final Thoughts

The monthly dividend stocks are primarily REITs and BDCs with a few other companies thrown into the mix. For those investors looking for decent yielding stocks that provide a monthly income stream, those companies highlighted in green in the spreadsheet above are likely your best option.

Of the monthly dividend stocks analyzed in this article, only Realty Income has a long enough dividend history to be eligible for the Sure Dividend database based on The 8 Rules of Dividend Investing.

Disclosure: This article was originally published on Sure Dividend by Dirk S. Leach.