It should come as no surprise to anyone that Tesla Inc (NASDAQ: TSLA) is back in the news, though it seems to be for all of the wrong reasons. From Musk’s Twitter escapades with the SEC, to talk about electric lawn blowers to concerns about a debt death spiral, the company has managed, yet again, to get in its own way, and this time, it has paid a price in the market, as its stock price tests lows not seen in a couple of years. I would be lying if I said that I do not find the company fascinating, and as has been my pattern for the last six years, it is time for a Tesla valuation update.

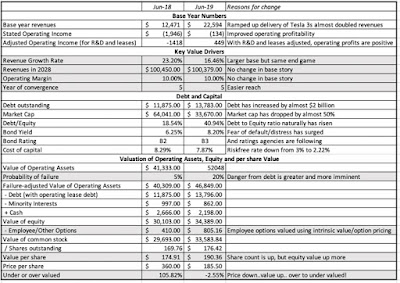

In my last valuation of Tesla, set in June 2018, I considered possible, plausible and probable valuations for the company. In my story, which I admitted was an optimistic one, I mapped out a pathway for the company to deliver $100 billion in revenues in 2028, while pushing pre-tax operating margins to 10% by 2023. The value that I obtained for the stock was $170-$180 per share, depending on how the very generous option package (20.2 million options) granted to Musk were treated, and is in the picture below:

In that post, I also listed possible, perhaps even plausible, scenarios where Tesla’s value per share could be higher than $400/share, but argued that it would require the equivalent of a royal flush for the company to get there, a combination of a ten-fold increase in revenues, an operating margin of 12% and reinvesting more like a technology than an automotive company. Since the stock was trading at close $360 at the time of the valuation, I concluded that it was significantly over valued. True to form, Elon Musk roiled the waters in August 2018 with his now infamous tweet about funding being secured for a $420 buyout of the stock, causing a surge in the stock price, before questions arose about both how secured the funding actually was and whether the $420 price itself was fiction.

In my post on the topic, I argued that if you were a private equity investor interested in taking a company private, Tesla would be a poor target, given its need for capital to keep growing, its heavy debt burden and the presence of Elon Musk as CEO. In the months after, both Musk and Tesla paid hefty prices for the indiscreet tweet, with the former in the SEC crosshairs for alleged stock price manipulation and the latter having to fight through the fog to get its story heard.

Catching up with the news

If you are wondering how much can happen in a year, you obviously don’t follow Tesla, since the company is a magnet for newsworthy events. Borrowing a movie title to categorize what’s happened to the company in the last year, I would break the news down into the good, the bad and what I can only term as gobsmacking, where you whack your head and say “what the heck was that?”

1. The Good

The market momentum has clearly shifted against Tesla, and all the news about the company seems to skew “bad”, it is worth noting that there are good things that have happened at the company over the last year:

Revenue Surge: In the drama around production targets and logistical misses, it is easy to lose sight of the fact that the Tesla 3 has caused the company to almost double revenues over the course of the last year, while easily winning the race for best selling electric car in the world.

Improving Profitability: While Musk’s tweets about Tesla turning earnings positive may have been premature, the company has moved down the pathway to profitability, reducing operating losses and with R&D capitalized, perhaps even turning the corner on operating profitability.

In short, the operating base on which I will be building my Tesla valuation in June 2019 will be a more solid one than the one that I was using in 2018.

We may use your email to send marketing emails about our services. Click here to read our privacy policy.

2. The Bad

With Tesla Inc (NASDAQ: TSLA), good news is always bundled with bad, some of it caused by macro events but much of it the consequence of self inflicted wounds:

Debt load and Distress: When Tesla chose to add to its debt burden by borrowing $5 billion in 2017, I argued that there was no good reason for Tesla to borrow money, since money losing companies gain no tax benefits and debt put growth potential at risk. Tesla has since added to that debt, using the false logic that it needed to borrow money to fund its growth; a much better option would have been to raise equity, the dilution bogeyman notwithstanding. In June 2019, that debt, now close to $14 billion, is revealing its dark side, as a bond price plunge and ratings downgrades threaten to put Tesla’s growth story at risk.

Reinvestment Lags: Growth requires reinvestment, and especially so for automobile companies, where assembly lines and logistical infrastructure need to be put in place for cars to be delivered to customers. It is both frustrating and puzzling that Tesla, a company with a loyal customer base that is willing to wait, has been unwilling to make the investments that it needs to meet the demand. Instead, the company seems to lurch from one production crisis to another one (remember the tents that had to be put up to reach the 5,000 cars/week target) while its CEO muddies the water further by arguing that the company is not just earnings positive but cash flow positive. At the moment, the Fremont plant remains Tesla’s major production facility, and while a plant in China is supposedly set for production late in 2019, the US/China trade war and Tesla’s own tangled history on operating delays leads to skepticism.

It is also worth noting that a significant part of Tesla’s time has been spent extracting itself from another unforced error, its acquisition of Solar City in 2016, with cost cuts and employee layoffs that are incongruent with a company claiming to tell a great growth story.

3. The Gobsmacking

An investor in Tesla should earn a special premium for having to endure news stories about the company that are so unusual that they would be considered fiction at other companies. Just to give a sampling, here are the other items that added to the smoke around the stock:

SEC Oversight: If there has been a recurring story over the past year, it has to do with the aftermath of Elon Musk’s “funding secured” tweet, which led to a SEC investigation and a threat of sanctions on the company. While the company came to a settlement wit the SEC, that settlement requires restraint on the part of Musk on future disclosures to the market (especially in the form on tweets), and restrain is not a Musk strong point.

Autonomous Cars: In April 2019, Musk unveiled a plan to roll out autonomous taxis, with Tesla owners being allowed to add to the network, in the near future, with the promise that Tesla’s technology on auto driving was well ahead of the competition. There is a debate worth having about autonomous cars and how they will change the ride sharing business, but it is almost certain that this will not happen smoothly or soon.

For the bulk of its existence, Tesla has been a story stock. That remains true, but as the company ages and acquires substance, you can argue that the story is getting more bounded. In this section, I will update my Tesla story and valuation first, then look at the uncertainty around the valuation and close with a comment on a “valuation” by ARK Invest, one of Tesla’s biggest institutional cheerleaders.

1. The Story: Tesla, Corporate Teenager?

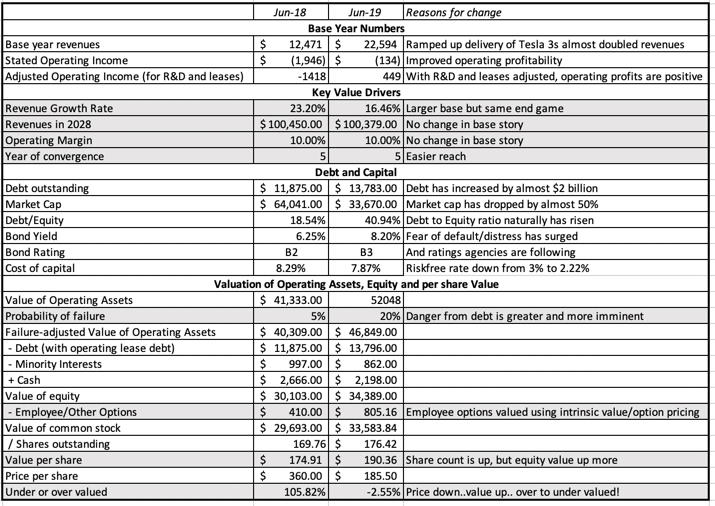

Bringing together everything that has happened at Tesla Inc (NASDAQ: TSLA) over the last year, I find myself telling the same story that I told about Tesla a year ago, of a company that would find a pathway to revenues of $100 billion in 2028, with strong operating margins, remains intact, with one notable change. The company’s debt overhang, already a concern a year ago, has become a clear and present danger to the company. In effect, on an operating basis, the company is in better shape than it was a year ago but on a financial leverage basis, it faces more truncation risk (a chance of failure of 20%). The value per share that I get with both effects built in is about $190/share:

If there is a modification to my story, it would be this. As I watched Musk repeatedly put Tesla’s story and value at risk with his distractions, I was reminded of teenagers around the world, with immense potential and intelligence, who risk it all for momentary and often meaningless rushes. In fact, I am tempted to add a corporate teenage phase in my corporate life cycle framework and put Tesla in it, a corporate teenager with immense potential, who repeated puts it all at risk for distractions.

To provide perspective on why the value per share today is higher, even with a much greater chance of failure, I compared the numbers that I used in my valuation in June 2018 to June 2019:

Note that while my end game on revenues ($100 billion by 2028) and operating margins (10% in 5 years) has not changed, the base numbers make both easier reaches. The rise in failure risk (from 5% in 2018 to 20% in 2019) is at least partially offset by a lower risk free rate and a cost of capital. In truth, the value per share is close enough that I would argue that there really has been little change, but the price per share has dropped by almost 50%, making the stock go from being significantly over valued to close to fairly valued now.

2. Facing up to Uncertainty

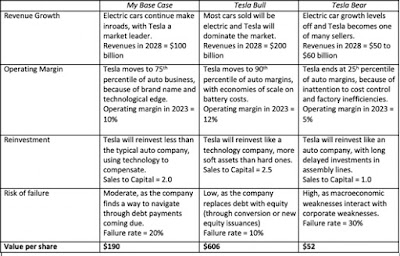

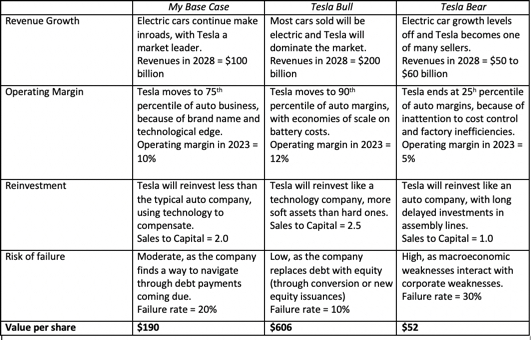

As with every Tesla valuation that I have done over the last six years, this one comes with caveats and uncertainties, and the contrasting views that bulls and bears have about the company are captured in the table below:

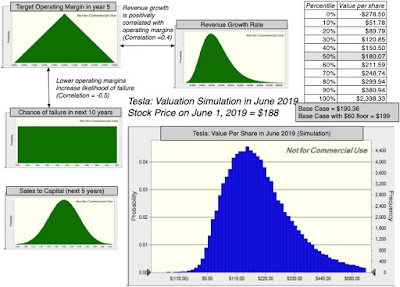

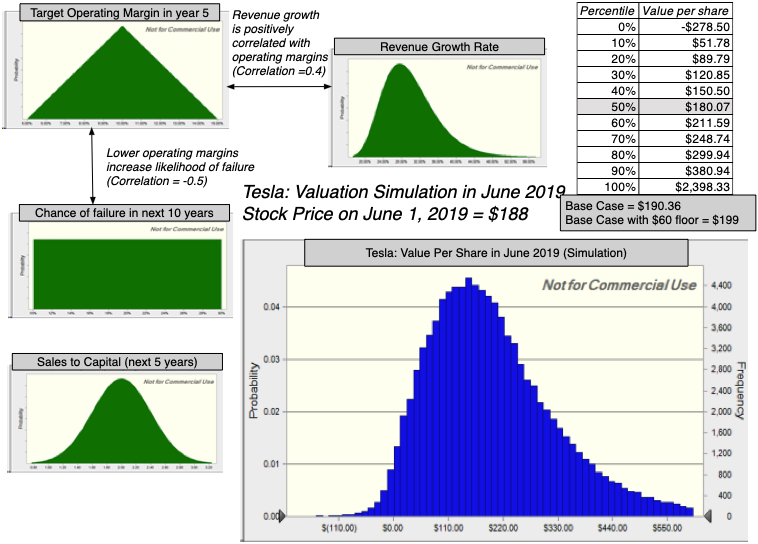

As you can see, I borrow from both sides of this debate, and I am sure that Tesla bulls will be disappointed that I don’t have higher revenues for the company and Tesla bears will take issue with my reinvestment assumptions and expectations that the company will eventually deliver solid margins. Using a technique that I find useful, when confronted with divergent views, to deal with uncertainties, I computed Tesla’s values in a simulation, with the results below:

in summary, the median value across the 100,000 simulations is $180/share, the 10th percentile delivering a $52 value/share and the 90th yielding $380/share. In this simulation, I have assumed that Tesla will remain a stand alone, going concern, and that the equity value could drop to zero, if there is a shock to the value of operating assets, given the debt load. There is talk, however, that Tesla could become an acquisition target, to an automobile company or a tech company (see this rumor about Apple being interested in 2014).

While there are some entanglements (such as the one with Panasonic in the battery factories) that will have to be worked out, there have generally been two impediments on this path. One is that Tesla has been an expensive target, especially when its market capitalization exceeded $50 billion. That will become less of a barrier, as the stock price drops, and at a market cap of less than $15 billion, it could be much more affordable. The other is a bigger and more intractable problem. With Elon Musk as part of the package, Tesla has a poison pill that few companies will want to imbibe, and it is likely that the relationship will have to be severed or at least significantly weakened for an acquisition to occur. I remain skeptical on the odds of an acquisition, precisely because I don’t see Musk going quietly into the night, but adding an acquisition floor at a $15 billion value for equity (about $60/share) increases the simulated value for the stock by about $10/share.

3. The ARK Tesla Pricing

It is not my role to be an arbiter of other people’s valuations, and I generally avoid commenting on them unless they are in the public domain, as was the case with the Tesla/Solar City fairness opinions, or seek public comment. I will make an exception with the ARK “valuation” of Tesla, partly because they are among the stock’s strongest boosters and partly because they put their model up for public comments, for which I commend them. In summary, here are the ARK numbers:

This is a pricing, not a valuation: I know that this will strike some as nitpicking but what ARK has produced is a forward pricing for Tesla, not a valuation. An intrinsic valuation requires forecasting cash flows over time, after taxes and reinvestment, and then discounting those cash flows back at a rate that reflects the risk in the investment. A pricing usually involves picking a metric (revenues, earnings, EBITDA), picking a forecast year for the metric and applying a multiple based upon what other companies in the peer group trade at. ARK’s basic model forecasts revenues, earnings and other metrics in 2023, and applies a multiple to estimated EBITDAR&D in 2023, making it a forward pricing.

The ARK bear is bullish: The ARK bear case requires that Tesla will sell 1.7 million cars in 2023, at an average price of $50,000/car and generate an operating margin of 6.1% on those revenues. Each of these assumptions is plausible, and the combination is possible, though to call a seven fold increase in revenues over five years, with a concurrent improvement to industry average profitability, a bear case seems to be stretching the definition of bear.

The weakest link: The model’s weakest link is on cash flows, since to sell 1.7 million cars, you have to make them first, and Tesla’s production capacity, even if you count the China plant as functional and about the same capacity as the Fremont plant, brings you only about half way to the goal. It will be magical, if adding another $3.7 billion to net PP&E (as ARK seems to be assuming) and $1.2 billion to working capital will allow you to increase revenues by $63.5 billion, but it gets even more stretched, when you assume that Tesla also pays off $14 billion in debt (as ARK seems to) over the five years. In sum, the bear case will require at the very least $25 to $30 billion in cash flows, even with ARK’s own assumptions, over the next five years, and since the operating cash flows at the company are still a trickle, this will require equity issuances in massive proportions fairly soon. ARK does allow for an equity capital raise of $10.6 billion which strikes me as too little to fill the gap, but in the absence of a balance sheet or statements of cash flows, I may be missing something (and it has to be very big).

Share count issue: Even for the equity capital raise of $10.6 billion, ARK reduces the impact on share count by assuming a stock price of $360/share (market cap will be $70 billion) at the time of the raise. Since this capital will have to be raised soon, there is an element of wishful thinking here, i.e., that stock prices will double in short order and the capital raise will follow. In addition, if stock prices do climb, as ARK assumes, there will there is an overhang of 20 million options that have been granted to Musk by the board of directors that will become actual shares. In short, for the ARK bear case to unfold, the share count will have to double over the next five years.

There is a time value question: Applying a multiple to EBITDAR&D in 2023 gives you a value in 2023, and to make it comparable to today’s stock price, you will have to discount it back to today, at a risk adjusted rate. In fact, if you bring in the probability of failure embedded in Tesla bonds, there will an additional discounting on value.

Even if you take the ARK bear case as realistic, with Tesla Inc (NASDAQ: TSLA) projected to sell 1.7 million cars in 2023 and earn operating margins close to the auto sector, the pricing per share that you get will be closer to $250/share, with a more realistic share count and time value adjustments, not the $560 that you see on the ARK spreadsheet. As for the bull case, I will leave it untouched, since it strikes me as more fairy tale than valuation, a world where there will be 7.2 autonomous cars on the road in 2023, with Tesla controlling a 70% market share, and generating $52 billion in annual cash flows. I am willing to accept the argument that Tesla is closer to mastering the autonomous car technology than its competitors, but I see a business that is further in the future than 2023, less dominated by Tesla and much less profitable than ARK is assuming it to be. In short, right now, it is more option than conventional going concern value, and even if I believed it, I would make more money selling short on Uber and Lyft, than buying Tesla.

Bottom Line

I did my first valuation of Tesla in 2013, and undershot the mark, partly because I saw its potential market as luxury cars (smaller), and partly because I under estimated how much it would be able to extract in production from the Fremont plant. Over time, I have compensated for both mistakes, giving Tesla access to a bigger (albeit, still upscale) market and more growth, while reinvesting less than the typical auto company. In spite of these adjustments, I have consistently come up with valuations well below the price, finding the stock to be valued at about half its price only a year ago.

This year marks a turning point, as I find Tesla to be under valued, albeit by only a small fraction. Even in the midst of my most negative posts on Tesla, I confessed that I like the company (though not Elon Musk’s antics as CEO and financial choices) and that I would one day own the stock. That day may be here, as I put in a limit buy order at $180/share, knowing fully well that, if I do end up as a shareholder, this company will test my patience and sanity. (Update: My limit buy just executed. As a shareholder my risks would be much lower, if Musk was banned from tweeting…)

When Jeff Bezos said that one breakthrough technology would shape Amazon’s destiny, even Wall Street’s biggest analysts were caught off guard.

Fast forward a year and Amazon’s new CEO Andy Jassy described generative AI as a “once-in-a-lifetime” technology that is already being used across Amazon to reinvent customer experiences.

At the 8th Future Investment Initiative conference, Elon Musk predicted that by 2040 there would be at least 10 billion humanoid robots, with each priced between $20,000 and $25,000.

Do the math. According to Musk, this technology could be worth $250 trillion by 2040.

Put another way, that’s roughly equal to:

175 Teslas

107 Amazons

140 Metas

84 Googles

65 Microsofts

And 55 Nvidias

And here’s the wild part — this $250 trillion wave isn’t tied to one company, but to an entire ecosystem of AI innovators set to reshape the global economy.

It’s a leap so massive, it could reshape how businesses, governments, and consumers operate worldwide.

Even if that $250 trillion figure sounds ambitious, major firms like PwC and McKinsey still see AI unlocking multi-trillion-dollar potential.

How could anything be worth that much?

The answer lies in a breakthrough so powerful it’s redefining how humanity works, learns, and creates.

And this breakthrough has already set off a frenzy among hedge funds and Wall Street’s top investors.

What most investors don’t realize is that one under-owned company holds the key to this $250 trillion revolution.

In fact, Verge argues this company’s supercheap AI technology should concern rivals.

Before I reveal the details, let’s talk about how some of the richest people on the planet are positioning themselves.

Bill Gates sees artificial intelligence as the “biggest technological advance in my lifetime,” more transformative than the internet or personal computer, capable of improving healthcare, education, and addressing climate change.

Larry Ellison — through Oracle, is spending billions on Nvidia chips and partnering with Cohere to embed generative AI across Oracle’s cloud and apps.

Warren Buffett — not known for tech hype — says this breakthrough could have a ‘hugely beneficial social impact.

When billionaires from Silicon Valley to Wall Street line up behind the same idea — you know it’s worth paying attention to.

Even as we admire what Tesla, Nvidia, Alphabet, and Microsoft have built, we believe an even greater opportunity lies elsewhere…

But the real story isn’t Nvidia — it’s a much smaller company quietly improving the critical technology that makes this entire revolution possible.

And judging by what I’m hearing from both Silicon Valley insiders and Wall Street veterans…

This prediction might not be bold at all:

A few years from now, you’ll wish you’d owned this stock.

The best part? You can discover everything about this company and its groundbreaking technology right now.

I’ve compiled everything you need to know about this groundbreaking company in a detailed, members-only report.

Trust me — you’ll want to read this report before putting another dollar into any tech stock.

For a ridiculously low price of just $9.99 a month, you can unlock a year’s worth of in-depth investment research and exclusive insights – that’s less than a single fast food meal!

Here’s why this is a deal you can’t afford to pass up:

• Access to our Detailed Report on this Game-Changing AI Stock: Our in-depth report dives deep into our #1 AI stock’s groundbreaking technology and massive growth potential.

• 11 New Issues of Our Premium Readership Newsletter: You will also receive 11 new issues and at least one new stock pick per month from our monthly newsletter’s portfolio over the next 12 months. These stocks are handpicked by our research director, Dr. Inan Dogan.

• One free upcoming issue of our 70+ page Quarterly Newsletter: A value of $149

• Bonus Reports: Premium access to members-only fund manager video interviews

• Ad-Free Browsing: Enjoy a year of investment research free from distracting banner and pop-up ads, allowing you to focus on uncovering the next big opportunity.

• 30-Day Money-Back Guarantee: If you’re not absolutely satisfied with our service, we’ll provide a full refund within 30 days, no questions asked.

If you’re thinking about getting in, don’t wait – because once Wall Street catches wind of this story, the easy money will be gone.

Space is Limited! Only 1000 spots are available for this exclusive offer. Don’t let this chance slip away – subscribe to our Premium Readership Newsletter today and unlock the potential for a life-changing investment.

Here’s what to do next:

1. Head over to our website and subscribe to our Premium Readership Newsletter for just $9.99 a month.

2. Enjoy a year of ad-free browsing, exclusive access to our in-depth report on the revolutionary AI company, and the upcoming issues of our Premium Readership Newsletter over the next 12 months.

3. Sit back, relax, and know that you’re backed by our ironclad 30-day money-back guarantee.

Don’t miss out on this incredible opportunity! Subscribe now and take control of your AI investment future!