In my time in corporate finance and valuation, I have seen many “new and revolutionary” ideas emerge, each one marketed as the solution to all of the problems that businesses face. Most of the time, these ideas start by repackaging an existing concept or measure and adding a couple of proprietary tweaks that are less improvement and more noise, then get acronyms, before being sold relentlessly. With each one, the magic fades once the limitations come to the surface, as they inevitably do, but not before consultants and bankers have been enriched. So, forgive me for being a cynic when it comes to the latest entrant in this game, where ESG (Environmental, Social and Governance), a measure of the environment and social impact of companies, has become one of the fastest growing movements in business and investing, and this time, the sales pitch is wider and deeper.

Companies that improve their social goodness standing will not only become more profitable and valuable over time, we are told, but they will also advance society’s best interests, thus resolving one of the fundamental conflicts of private enterprise, while also enriching investors. This week, the ESG debate has come back to take main stage, for three reasons.

– It is the fiftieth anniversary of one of the most influential opinion pieces in media history, where Milton Friedman argued that the focus of a company should be profitability, not social good. There have been many retrospectives published in the last week, with the primary intent of showing how far the business world has moved away from Friedman’s views.

– There were multiple news stories about how “good” companies, with goodness measured on the social scale, have done better during the COVID crisis, and how much money was flowing into ESG funds, with some suggesting that the crisis could be a tipping point for companies and investors, who were on the fence about the added benefits of being socially conscious.

– In a more long standing story line, the establishment seems to have bought into ESG consciousness, with business leaders in the Conference Board signing on to a “stakeholder interest” statement last year and institutional investors shifting more money into ESG funds.

lassedesignen/Shutterstock.com

In the interests of openness, I took issue with the Conference Board last year on stakeholder interests, and I start from a position of skepticism, when presented with “new” ways of business thinking. If the debate about ESG had been about facts, data and common sense, and ESG had won, I would gladly incorporate that thinking into my views on corporate finance, investing and valuation. But that has not been the case, at least so far, simply because ESG has been posited by its advocates as good, and any dissent from the party line on ESG (that it is good for companies, investors and society) is viewed as a sign of moral deficiency. At the risk of sounding being labeled a troglodyte (I kind of like that label), I will argue that many fundamental questions about ESG have remained unanswered or have been answered sloppily, and that it is in its proponents’ best interests to stop overplaying the morality card, and to have an honest discussion about whether ESG is a net good for companies, investors and society.

Measures of Goodness

We have spent decades measuring financial performance and output at companies, either at the operating level, as revenues, profits or capital invested, or at the investor level, as market cap and returns. Any attempts to measure environment and social goodness face two challenges.

– The first is that much of social impact is qualitative, and developing a numerical value for that impact is difficult to do.

– The second is even trickier, which is that there is little consensus on what social impacts to measure, and the weights to assign to them.

If your counter is that there are multiple services now that measure ESG at companies, you are right, but the lack of clarity and consensus results in the companies being ranked very differently by different services. This shows up in low correlations across the ESG services on ESG scores, as indicated by this study:

|

| Correlations across six ESG data providers |

This low correlation often occurs even on high profile companies, as shown in a comprehensive analysis of ESG investing by Dimson, Marsh and Staunton, as part of their global investment returns update:

|

| Source: CS Global Investment Returns Yearbook 2020, Dimson, Marsh and Staunton |

Note the divergence in both the overall ratings and on the individual metrics (E, S and G) across the services, even for widely tracked companies like Facebook and Walmart. There are some who believe that this reflects a measurement process that is still evolving, and that as companies provide more disclosure on ESG data and ESG measurement services mature, there will be consensus. I don’t believe it! After all, what I find to be good or bad in a company will reflect my personal values and morality scales, and the choices I make will be different from your choices, and any notion that there will be consensus on these measures is a pipe dream.

Even if you overlook disagreements on ESG as growing pains, there is one more component that adds noise to the mix and that is the direction of causality: Do companies perform better because they are socially conscious (good) companies, or do companies that are doing well find it easier to do good? Put simply, if ESG metrics are based upon actions/measures that companies that are doing better, either operationally and/or in markets, can perform/deliver more easily than companies that are doing badly, researchers will find that ESG and performance move together, but it is not ESG that is causing good performance, but good performance which is allowing companies to be socially good.

The ESG Sales Pitch – Promises and Contradictions

The power of the ESG sales pitch has always been that it offers something good to everyone involved, from companies adopting its practices, to investors in those companies, and more broadly, to all of society.

– For companies, the promise is that being “good” will generate higher profits for the company, at least in the long term, with lower risk, and thus make them more valuable businesses.

– For investors in these companies, the promise is that investing in “good” companies will generate higher returns than investing in “bad” or middling companies.

– For society, the promise is that not only will good companies help fight problems directly related to ESG, like climate change and low wages, but also counter more general problems like income inequality and uneven healthcare.

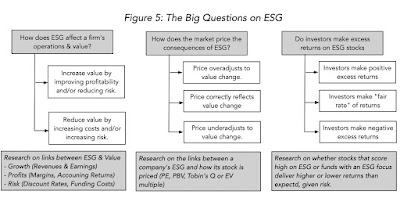

Given that ESG has been marketed as all things good, to all people, it is no surprise that its usage has soared, with companies signing on in droves to social compacts, and investors pouring hundreds of billions of dollars into ESG funds and investments. In the process, though, its advocates have either glossed over, or mixed up, three separate questions that need to be answered, on ESG:

The reason it is useful to separate the three questions is that it opens up possibilities that are often missed in both debate and research. For instance, it is possible that ESG does nothing for value, but that it offers a sheen to companies that allows them to be priced more highly than their less socially conscious counterparts and enriches investors, who trade on its basis. Alternatively, it is also possible that ESG does increase value, but that markets adjust quickly to this and that investors do not benefit from investing in ESG stocks. It also illustrates the danger of overreach from ESG research. Much of the research on ESG is compartmentalized, where only one of these questions is addressed, but the researchers seem to use the results to draw conclusions about answers the other two. Thus, a research study that finds that investors make higher returns on companies that rank high on ESG often will go on to posit that this must mean that ESG increases value, a leap that is neither justified nor warranted.

ESG and Value

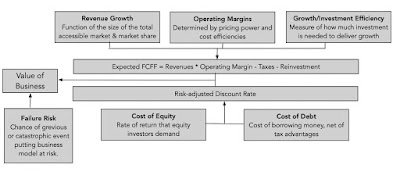

The framework for answering the question of whether ESG affects value is no different from the framework for assessing whether acquisitions or financing or any other action affects value. It is both simple and universal, and I have captured the drivers of value for any business in the picture below:

|

| Figure 1: The Drivers of Value |

In fact, my favorite propositions in value is the “It Proposition”, which posits that for “it” (investing, financing, dividends, ESG) to affect value, “it” has to affect either the cash flows (through revenue growth, operating margins and investment efficiency) or the risk in those cash flows (which plays out in the cost of equity and capital).

Goodness will be rewarded

Applying this proposition to ESG, the most direct way to induce companies to behave in a socially responsible manner is to make it in their financial best interests to do so. There is a plausible scenario, where being good creates a cycle of positive outcomes, which makes the company more valuable. Figure 2 describes this virtuous cycle:

In this story, being good benefits the company on multiple dimensions. Customers, attracted by the company’s social mission, are more likely to buy its products and pay higher prices, increasing both growth and margins. The company is able to attract more loyal employees and suppliers, and build a model for investing that leads to more payoff from investments, i.e., more efficient growth. On the risk front, the company benefits from investors who are willing to pay premium prices for their shares (thus lowering cost of equity), and lending that comes with lower rates and fewer covenants. Finally, by operating as a good corporate citizen, the company minimizes the chance of a scandal or a catastrophic event that could put its business model at risk. In the language of ESG, it creates a more “sustainable business”. For proponents of corporate social responsibility, this is the best-case setting for their cause, because being good and doing well financially converge. This scenario holds, though, only because customers, employees, investors, and lenders all put their money where their convictions lie, and are willing to make sacrifices along the way, and it is more likely in some companies/businesses than others:

- Smaller, rather than larger: While it is not impossible for a large company to hit all the high notes in the virtuous cycle, it is far easier for a small company than a large one, because even a small subset of all investors (consumers) can provide the capital (revenues) at the favorable terms needed for this scenario to unfold.

- Niche business, with a more socially conscious customer base: Adding to the smallness theme, it is easier for a company that serves a small customer base to attract customers with its ‘good company’ mantle than a company that seeks to reach a mass market. A company like Patagonia, with revenues of $750 million, can more easily make the compromises to stay socially responsible than a company like Nike, with revenues of $34 billion, which will be forced to make compromises that will undercut its goodness.

- A privately held company or a public company with an investor base that values corporate goodness and prices it in: Being a private company can help, especially if the payoff to corporate goodness is long term, another point working in Patagonia’s favor. A public company that is closely held or controlled by its founders can also make choices that may not be feasible for a widely held company with a vocal stockholder base.

It is worth noting that the companies that tend to be most vociferous about their social consciences tend to meet these criteria, at least early in their corporate lives. However, they will face a challenge, if they are successful and want to grow, because growth will bring in customers and investors not so committed to ESG. The acid test of social consciousness occurs when a company scales up and must decide whether to continue to grow or accept a lower ceiling on growth, and perhaps lower value, in order to preserve it good company status.

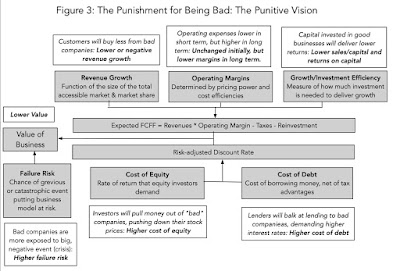

Badness will be punished

There is an alternate story that can be used to argue that companies should try to be socially responsible, but it is a more punitive one, where it is not good companies that get rewarded, but bad ones that get punished. This less upbeat scenario is described below:

Here, the punishment for bad companies is meted out from every direction, with customers refusing to buy their products, even if they are lower priced. These companies face higher operating expenses (and lower margins) in the long term, as they have trouble holding on to employees and finding suppliers. Equity investors avoid buying their shares, leading to higher costs of equity, and lenders are leery about lending money to these companies, leading to higher costs of debt. Finally, these companies risk exposure to grievous, or even catastrophic events, arising from operating with too little consideration of societal costs. It is often these events, such as the Union Carbide gas leak in Bhopal, Vale’s dam bursting in Bhopal and BP’s oil spill in the Gulf of Mexico, that highlight shortcomings and create long term problems for the company.

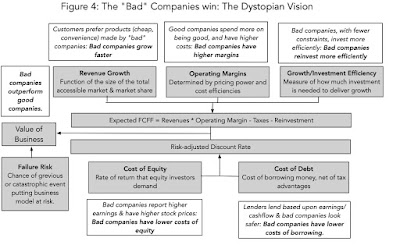

The Bad Guys win!

With regard to promoting social responsibility, the “bad behavior gets punished” scenario is not as good as the virtuous cycle, because it will tend to scare companies away from being “bad”, rather than induce them to be “good”, but it is still better than a third and potentially devastating scenario for ESG advocates, where bad companies are rewarded for being bad, and become more valuable than good ones:

In this scenario, bad companies mouth platitudes about social responsibility and environmental consciousness without taking any real action, but customers buy their products and services, either because they are cheaper or because of convenience, employees continue to work for them because they can earn more at these companies or have no options, and investors buy their shares because they deliver higher profits. As a result, bad companies may score low on corporate responsibility scales, but they will score high on profitability and stock price performance.

The Evidence

The question of which of these three scenarios is the right one is not one that can be settled by logic or with anecdotal evidence, but with data. For more than two decades now, researchers have examined the link, with the following conclusions:

- A Weak Link to Profitability: There are meta studies (summaries of all other studies) that summarize hundreds of ESG research papers, and find a small positive link between ESG and profitability, but one that is very sensitive to how profits are measured and over what period, leading one of these studies to conclude that “citizens looking for solutions from any quarter to cure society’s pressing ills ought not appeal to financial returns alone to mobilize corporate involvement”. Breaking down ESG into its component parts, some studies find that environment (E) offered the strongest positive link to performance and social (S) the weakest, with governance (G) falling in the middle.

- A Stronger Link to Funding Costs: Studies of “sin” stocks, i.e., companies involved in businesses such as producing alcohol, tobacco, and gaming, find that these stocks are less commonly held by institutions, and that they face higher costs for funding, from equity and debt). The evidence for this is strongest in sectors like tobacco (starting in the 1990s) and fossil fuels (especially in the last decade), but these findings come with a troubling catch. While these companies face higher costs, and have lower value, investors in these companies will generate higher returns from holding these stocks.

- And a link to Failure/Disaster Risk: An alternate reason why companies would want to be “good” is that “bad” companies are exposed to disaster risks, where a combination of missteps by the company, luck, and a failure to build in enough protective controls (because they cost too much) can cause a disaster, either in human or financial terms. That disaster can not only cause substantial losses for the company, but the collateral reputation damage created can have long term consequences. One study created a value-weighted portfolio of controversial firms that had a history of violating ESG rules, and reported negative excess returns of 3.5% on this portfolio, even after controlling for risk, industry, and company characteristics. The conclusion in this study was that these lower excess returns are evidence that being socially irresponsible is costly for firms, and that markets do not fully incorporate the consequences of bad corporate behavior. The push back from skeptics is that not all firms that behave badly get embroiled in controversy, and it is possible that looking at just firms that are controversial creates a selection bias that explains the negative returns.

In summary, based upon the studies so far, the strongest evidence in support of ESG seems to be that “bad” companies face higher funding costs (from debt and equity), whereas the evidence on ESG paying off as higher profits and growth is elusive. There is some evidence supporting the proposition that being socially responsible (or at least not being socially irresponsible) can protect companies from damaging disasters, but selection bias is a problem.

ESG and Returns

To begin with, the notion that adding an ESG constraint to investing increases expected returns is counter intuitive. After all, a constrained optimum can, at best, match an unconstrained one, and most of the time, the constraint will create a cost. In one of the few cases where honesty seems to have prevailed over platitudes, the TIAA-CREF Social Choice Equity Fund explicitly acknowledges this cost and uses it to explain its underperformance, stating that “The CREF Social Choice Account returned 13.88 percent for the year [2017] compared with the 14.34 percent return of its composite benchmark … Because of its ESG criteria, the Account did not invest in a number of stocks and bonds … the net effect was that the Account underperformed its benchmark.” In fact, there is an inherent contradiction, at least on the surface, between the argument that ESG leads to higher value and stock prices, made to CEOs and CFOs of companies, and a simultaneous argument that investors in ESG stocks will earn higher (positive excess) returns, by investing in these companies.

Value, Price and Returns: The Interplay

Whatever your beliefs may be on whether ESG increases or decreases value, you have to start with a fresh slate, and incorporate market behavior, to make judgments on whether investors will benefit from ESG investing, as can be seen in the table below:

Consider the first outcome, where ESG increases the value of a company, but markets overreact to the goodness of the company, pushing up the price too much: investors in good companies will earn lower returns (negative excess) returns over the long term. Flipped around, this table also yields the counter intuitive result that studies that conclude that ESG investing earns positive (or negative) returns tell us nothing or very little about the underlying benefits of ESG, since the market acts as the intervening variable.

The Evidence on ESG and Returns

It should come as no surprise then, that the research on the link between ESG and investor returns comes to split results:

– Invest in bad companies: There are the studies that we referenced earlier as backing for good firms having lower discount rates, including the ones that showed that sin stocks deliver higher returns than socially conscious companies. A comparison of two Vanguard Index funds, the Vice fund (invested in tobacco, gambling, and defense companies) and the FTSE Social Index fund (invested in companies screened for good corporate behavior on multiple dimensions) and note that a dollar invested in the former in August 2002 would have been worth almost 20% more by 2015 than a dollar invested in the latter.

– Invest in good companies: At the other end of the spectrum, there are studies that seem to indicate that there are positive excess returns to investing in good companies. A study showed that stocks in the Anno Domini Index (of socially conscious companies) outperformed the market, but that the outperformance was more due to factor and industry tilts than to social responsiveness. In a different study, researchers looked at the payoff to socially responsible investing by comparing the returns on two portfolios, created based upon eco-efficiency scores, and concluded that companies that are more eco-efficient generate higher returns. Some of the strongest links between returns and ESG come from the governance portion, which, as we noted earlier, is ironic, because the essence of governance, at least as measured in most of these studies, is fealty to shareholder rights, which is at odds with the current ESG framework that pushes for a stakeholder perspective.

– ESG has no effect: Splitting the difference, there are other studies that find little or no differences in returns between good and bad companies. A Morningstar Quantitative study of ESG stocks in 2020 found that companies that scored high on ESG generated mildly lower returns than companies that scored poorly, though the difference was statistically insignificant. In fact, studies that more broadly look at factors that have driven stock returns for the last few decades find that much of the positive payoff attributed to ESG comes from its correlation with momentum and growth.

In steady state, it is internally inconsistent to argue that good companies will benefit from lower funding costs (lower costs of equity) and that investors can also earn higher returns at the same time.

Glimmers of Hope for ESG Investing

There are two possible scenarios where being good may benefit both the company (by increasing its value) and investors in the company (by delivering higher returns).

- Transition Period Payoff: The first scenario requires an adjustment period, where being good increases value, but investors are slow to price in this reality. During the adjustment period the highly rated ESG stocks will outperform the low ESG stocks, as markets slowly incorporate ESG effects, but that is a one-time adjustment. Once prices reach equilibrium, highly rated ESG stocks will have greater values, but investors will have to be satisfied with lower expected returns. The presence of a transition period, where markets learn about ESG and price them in can also explain why there may be a payoff to more disclosure and transparency on social and environmental issues, by speeding the adjustment. It is perhaps this hope of transition period excess returns that that has driven some institutional investors to become more activist on ESG issues and can explain why some have been able to show excess returns from increasing (reducing) their holdings in good (bad) companies. It is not just the large players like Blackrock and Vanguard that have jumped on this bandwagon, but also pure return-focused investors like Elliott Management and Third Point which recently targeted utility companies about their excessive carbon footprints. Their activism goes well beyond jawboning management and includes efforts that range from stopping mergers to proxy fights to altering boards of directors. This study examined 613 public firms that were targeted by an activist institutional investor focused on improving ESG practices and found positive excess returns in the 18% of engagements where the activism succeeded.

- Limit Downside: The other scenario where incorporating ESG into investing may yield a payoff is when investors are concerned about limiting downside risk. To the extent that socially responsible companies are less likely to be caught up in controversy and to court disaster, the argument is that they will also have less downside risk than their counterparts who are less careful. There is some evidence of this in this paper that finds that companies that adopt better ESG practices are less likely to see large drops in value.

If there is an investing lesson embedded here, it is the unsurprising one that investors who hope to benefit from ESG cannot do so by investing mechanically in companies that already identified as good (or bad), but have to adopt a more dynamic strategy built around either aspects of corporate social responsibility that are not easily measured and captured in scores, or from getting ahead of the market in recognizing aspects of corporate behavior that will hurt the company in the long term.

The COVID effect

The last few months have been a test of ESG investing, and while the consensus view seems to be that ESG has passed the test, it is worth separating the facts from what is debatable.

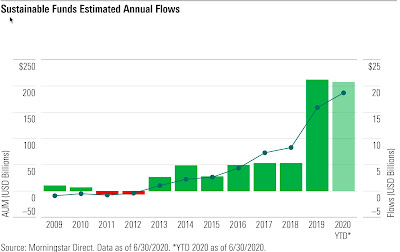

– Fund Flows (not debatable): It is not debatable that investors, whatever their reasons, have been investing more in ESG funds, both passively (through index funds) and actively (through ESG funds that contend that they can do better than the market). By early September 2020, impact investing index funds had risen to $250 billion in the US and more than a trillion dollars globally, with both numbers rising over the course of the COVID months.

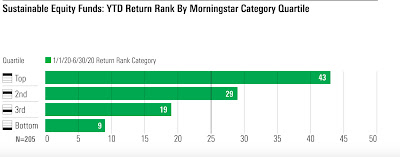

– Performance (debatable): The question of whether ESG funds have outperformed during the COVID crisis is more debatable. Early in the crisis, Blackrock asserted that sustainable investing had shown its value added, pointing to the fact that ESG indices were outperforming their market counterparts during the crisis months. The problem, though, is that Blackrock is not a neutral commenter on this issue, partly because Larry Fink has been a vocal salesman for ESG and partly because Blackrock has ESG products to sell. It is true that Morningstar seems to provide backing for this proposition, when they presented the results on ESG funds during the first half of 2020:

– Morningstar noted that ESG funds in all 26 categories that they track outperformed their conventional index fund counterparts. The consensus view that ESG investing outperformed the market is now getting push back, with this paper arguing that once you control for the sector tilt of ESG funds (they tend to be more heavily invested in tech companies), ESG, by itself, provided no added payoff during the down period of the crisis (February and March 2020) and pushed returns down during the recovery phase.

If success in active investing is defined as attracting investor money, ESG has had a successful run during COVID, but if it is defined as delivering returns, it is far too early to be doing victory dances in the end zone.

The Bottom Line

In many circles, ESG is being marketed as not only good for society, but good for companies and for investors. In my view, the hype regarding ESG has vastly outrun the reality of both what it is, and what it can deliver, and the buzzwords are not helpful. That is the reason I have tried to under use words like sustainability and resilience, two standouts in the ESG advocates lexicon, in writing this post. I believe that the potential to make money on ESG for consultants, bankers and investment managers has made at least some of them cheerleaders for the concept, with claims of the payoffs based on research that is ambiguous and inconclusive, if not outright inconsistent. The evidence as I see it is nuanced, and can be summarized as follows:

– There is a weak link between ESG and operating performance (growth and profitability), and while some firms benefit from being good, many do not. Telling firms that being socially responsible will deliver higher growth, profits and value is false advertising. The evidence is stronger that bad firms get punished, either with higher funding costs or with a greater incidence of disasters and shocks. ESG advocates are on much stronger ground telling companies not to be bad, than telling companies to be good. In short, expensive gestures by publicly traded companies to make themselves look “good” are futile, both in terms of improving performance and delivering returns.

– The evidence that investors can generate positive excess returns with ESG-focused investing is weak, and there is no evidence that active ESG investing does any better than passive ESG investing, echoing a finding in much of active investing literature. Even the most favorable evidence on ESG investing fails to solve the causation problem. Based on the evidence, it appears to me that just as likely that successful firms adopt the ESG mantle, as it is that adopting the ESG mantle makes firms successful.

– If there is a hopeful note for ESG investing, it is in the payoff to being early to the ESG game. Investors who are ahead of markets in assessing how corporate behavior, good or bad, will play out in performance or priced, will be able to earn excess returns, and if they can affect the change, by being activist, can benefit even more.

Much of the ESG literature starts with an almost perfunctory dismissal of Milton Friedman’s thesis that companies should focus on delivering profits and value to their shareholders, rather than play the role of social policy makers. The more that I examine the arguments that advocates for ESG make for why companies should expand mission statements, and the evidence that they offer for the proposition, the more I am inclined to side with Friedman. After all, if ESG proponents are right, and being good makes companies more profitable and valuable, they are on the same page as Friedman. If, on the other hand, adopting ESG practices makes companies less valuable, the onus is on ESG’s proponents to show that societal benefits exceed that lost value.

The ESG bandwagon may be gathering speed and getting companies and investors on board, but when all is said and done, a lot of money will have been spent, a few people (consultants, ESG experts, ESG measurers) will have benefitted, but companies will not be any more socially responsible than they were before ESG entered the business lexicon. What is needed is an open, frank, and detailed dialogue concerning ESG-related corporate policies, with an acceptance that being good can add value at some companies and may destroy value at others, and that in the long term, investing in good companies can pay off during transition periods but will often translate into lower returns in the long term, rather than higher returns.

YouTube Video

Paper on ESG (with Brad Cornell)

My blog posts on stakeholder wealth maximization

Disclosure: None.