In fact, my favorite propositions in value is the “It Proposition”, which posits that for “it” (investing, financing, dividends, ESG) to affect value, “it” has to affect either the cash flows (through revenue growth, operating margins and investment efficiency) or the risk in those cash flows (which plays out in the cost of equity and capital).

Goodness will be rewarded

Applying this proposition to ESG, the most direct way to induce companies to behave in a socially responsible manner is to make it in their financial best interests to do so. There is a plausible scenario, where being good creates a cycle of positive outcomes, which makes the company more valuable. Figure 2 describes this virtuous cycle:

In this story, being good benefits the company on multiple dimensions. Customers, attracted by the company’s social mission, are more likely to buy its products and pay higher prices, increasing both growth and margins. The company is able to attract more loyal employees and suppliers, and build a model for investing that leads to more payoff from investments, i.e., more efficient growth. On the risk front, the company benefits from investors who are willing to pay premium prices for their shares (thus lowering cost of equity), and lending that comes with lower rates and fewer covenants. Finally, by operating as a good corporate citizen, the company minimizes the chance of a scandal or a catastrophic event that could put its business model at risk. In the language of ESG, it creates a more “sustainable business”. For proponents of corporate social responsibility, this is the best-case setting for their cause, because being good and doing well financially converge. This scenario holds, though, only because customers, employees, investors, and lenders all put their money where their convictions lie, and are willing to make sacrifices along the way, and it is more likely in some companies/businesses than others:

- Smaller, rather than larger: While it is not impossible for a large company to hit all the high notes in the virtuous cycle, it is far easier for a small company than a large one, because even a small subset of all investors (consumers) can provide the capital (revenues) at the favorable terms needed for this scenario to unfold.

- Niche business, with a more socially conscious customer base: Adding to the smallness theme, it is easier for a company that serves a small customer base to attract customers with its ‘good company’ mantle than a company that seeks to reach a mass market. A company like Patagonia, with revenues of $750 million, can more easily make the compromises to stay socially responsible than a company like Nike, with revenues of $34 billion, which will be forced to make compromises that will undercut its goodness.

- A privately held company or a public company with an investor base that values corporate goodness and prices it in: Being a private company can help, especially if the payoff to corporate goodness is long term, another point working in Patagonia’s favor. A public company that is closely held or controlled by its founders can also make choices that may not be feasible for a widely held company with a vocal stockholder base.

It is worth noting that the companies that tend to be most vociferous about their social consciences tend to meet these criteria, at least early in their corporate lives. However, they will face a challenge, if they are successful and want to grow, because growth will bring in customers and investors not so committed to ESG. The acid test of social consciousness occurs when a company scales up and must decide whether to continue to grow or accept a lower ceiling on growth, and perhaps lower value, in order to preserve it good company status.

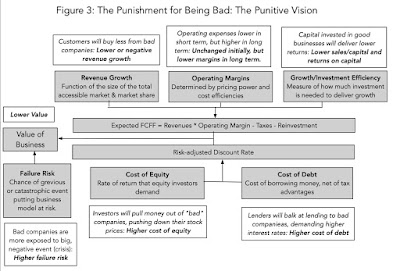

Badness will be punished

There is an alternate story that can be used to argue that companies should try to be socially responsible, but it is a more punitive one, where it is not good companies that get rewarded, but bad ones that get punished. This less upbeat scenario is described below:

Here, the punishment for bad companies is meted out from every direction, with customers refusing to buy their products, even if they are lower priced. These companies face higher operating expenses (and lower margins) in the long term, as they have trouble holding on to employees and finding suppliers. Equity investors avoid buying their shares, leading to higher costs of equity, and lenders are leery about lending money to these companies, leading to higher costs of debt. Finally, these companies risk exposure to grievous, or even catastrophic events, arising from operating with too little consideration of societal costs. It is often these events, such as the Union Carbide gas leak in Bhopal, Vale’s dam bursting in Bhopal and BP’s oil spill in the Gulf of Mexico, that highlight shortcomings and create long term problems for the company.