The Video On Demand (systems by which users select and watch video content on demand) market is becoming more and more attractive. Since 2010, new competitors, from start-ups to gigantic entertainment content companies, have joined the game. This has caused the market to be more competitive, as competitors fight for distributing more content, increasing video quality (high definition) and download speed and reducing their subscription fees.

But this is just the beginning. In order to become future market leaders and attract more subscribers, some competitors are making huge investments, as you will see later. After all, the market leader will not only enjoy several competitive advantages in terms of cost efficiency, but it will also have the biggest exposure to a very promising and huge market: in September 2012, Nielsen mentioned that 162 million Americans watched online video. They spent almost seven hours of the month viewing content, streaming nearly 26 billion videos.

Furthermore, the U.S. is just an example of how far video streaming penetration can go in an economy. As users in Europe and emerging markets in Asia and Latin America shift from TV to video on demand, the international market for video streaming is even more attractive. Any company that succeeds in expanding its video services internationally is set to experience amazing revenue growth rates for the next three years. But, who will win the war for the video streaming market?

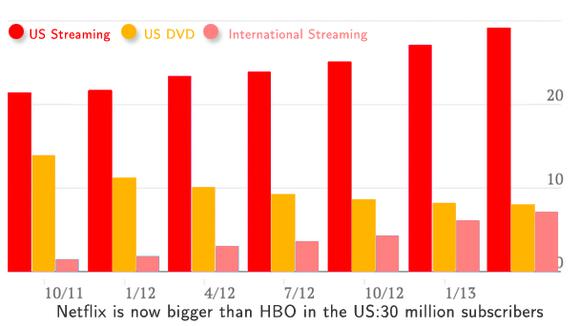

Netflix, Inc. (NASDAQ:NFLX) : Now Bigger than HBO

Netflix, Inc. (NASDAQ:NFLX) is an early mover. It wisely used cash from its DVD rental business to enter into the streaming business in the U.S. some years ago, and this move proved to be very successful Now, Netflix has more than 32 million subscribers in the U.S., Canada, Latin America, Ireland, and the United Kingdom. Even better, there is room for further growth, not only abroad.

In the U.S., Americans still watch more than eight hours of television per day (Nielsen). As Americans continue shifting to video on demand, Netflix, Inc. (NASDAQ:NFLX) is likely to attract many new customers with its huge content database. In the last quarter, Netflix, Inc. (NASDAQ:NFLX) added 2 million new members in the U.S. and roughly 1 million new members abroad.

Although Netflix, Inc. (NASDAQ:NFLX)’s growth has been amazing, the company has several challenges to face from now on. First of all, Netflix is able to capture customers because of its large content database: without content, Netflix would not be able to survive. This puts limits on Netflix’s profitability and adds risks due to the uncertainty of negotiations with content providers in the future. Netflix has a relatively larger content budget relative to the competition.

In many cases, the company might be overpaying for content, while Amazon.com, Inc. (NASDAQ:AMZN) and Hulu are not. Also, Netflix is already so big that it is relying on emerging markets to continue promising outstanding revenue growth to investors. We don’t know for sure if these markets will be profitable in the medium run, because content providers in these markets are also interested in providing their own video streaming service (like Televisa in Mexico) and would only sell their content for elevated fees.

Amazon Prime may be the next big thing

If there is somebody who knows about permanent innovation and expansion, that’s Amazon.com, Inc. (NASDAQ:AMZN). From books to server farms (Amazon Web Services), and now from server farms to video streaming and beyond. Amazon Prime is the product designed to compete against Netflix for video demand: Prime members enjoy free two days shipping on millions of items with their purchase, unlimited instant streaming of thousands of movies and TV shows, and a Kindle book to borrow for free each month. Once more, Amazon.com, Inc. (NASDAQ:AMZN) is using the resources from other successful products to market a new one.

Amazon.com, Inc. (NASDAQ:AMZN) is also well aware of the importance that content abundance has in this market. But it is not paying too much for it. The company knows its limits. In two years and a half, the company multiplied by 20 the number of videos and materials available for Prime users. Finally, Amazon.com, Inc. (NASDAQ:AMZN) Prime is cheaper: the $79 annual Prime membership fee is $17 less than the $96 Netflix members spend for streaming (per year).

Comcast Corporation (NASDAQ:CMCSA) : It’s never late to join the party

Comcast Corporation (NASDAQ:CMCSA) is not a video streaming company. It is a global media and tech company with a strong cable TV revenue component: around 35% of Comcast Corporation (NASDAQ:CMCSA)’s value. But as customers shift to video on demand and satellite companies, Comcast realized it had to change its business if it wanted to survive the next five years. As a result, the company started diversifying business segments, including broadcast television, cable networks, and even theme parks.

Acquiring media corporation NBC Universal last year gave Comcast Corporation (NASDAQ:CMCSA) more exposure to the broadcast network business, international cable networks, and operations of Universal Pictures in the production, acquisition, and distribution of films globally. In other words, Comcast Corporation (NASDAQ:CMCSA) owns top quality content and has excellent contacts and relations with broadcast networks.

Therefore, it made a lot of sense for Comcast to launch Xfinity TV, its own video streaming service. That being said, the product sells TV series , while Netflix is more about movies. Also, because Comcast’s cash cow is the cable business, the more progress Netflix and Amazon Prime make, the worse for Comcast’s cable business, as cable and video on demand through Internet are becoming substitutes for most users. The acquisition of NBCU adds exposure to this threat.

The bottom line

In this article, I analyzed three examples of companies fighting for market share in the promising video streaming market: an early mover (Netflix), an internet company with enough resources to make its product more competitive and attractive (Amazon), and a big global media corporation trying to join the party late and make its traditional services more protected against video on demand. There are, naturally, many more competitors, like Hulu, but I think the group I chose represents well the categories of players in this market.

While Netflix is the king in terms of content database size, Amazon is growing fast. Comcast, on the other hand, is too exposed to traditional and already mature markets, like the cable business, and regardless of Xfinity TV, this will continue having an overall negative influence on revenue growth. I tend to think that Amazon Prime has more opportunities for expansion in the coming years, since Amazon can offer something “more than streaming” with Prime: Kindle subscriptions, benefits on the online store, etc.

This will bring more customers, nationally and internationally. Also, the company can use the contacts and experience it has after internationalizing successfully its market place, to make Amazon Prime a leading video streaming choice in emerging markets. It seems that Amazon can become a leader not only in online e-commerce or server farms, but also in video streaming.

Adrian Campos has no position in any stocks mentioned. The Motley Fool recommends Amazon.com and Netflix. The Motley Fool owns shares of Amazon.com and Netflix.

The article Who Will Win the War for the Video Streaming Market? originally appeared on Fool.com and is written by Adrian Campos.

Adrian is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.