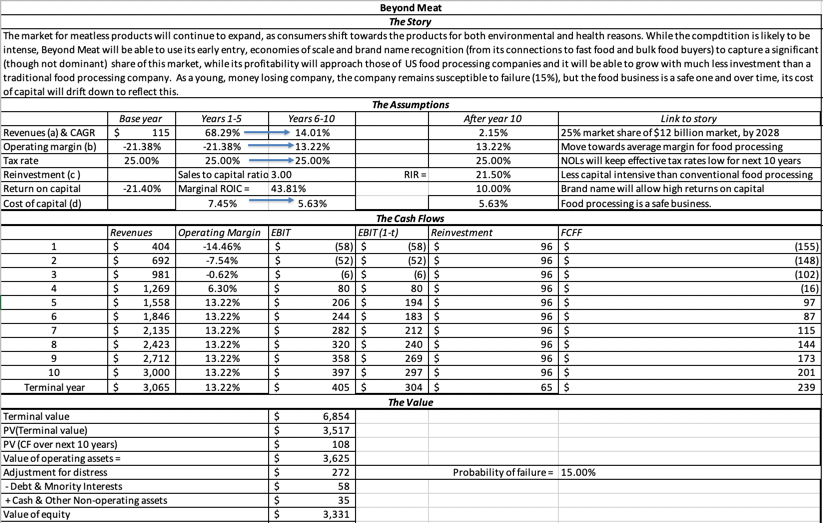

Is there risk in this investment? Absolutely, and you may be surprised that my cost of capital is only 7.46%, but that reflects my assessment of risk in this investment, as a going concern and as part of a diversified portfolio. As a money-losing company that will require about $500 million in capital over the next four years to deliver on its potential, there remains a significant chance of failure, and I estimate the probability of failure to be 15%.

The Valuation: With the story in place, the valuation follows and the picture below captures the ingredients of value:

|

| Download spreadsheet |

With my story, which I believe reflects an upbeat story for the company, the value that I obtain for its equity is $3.3 billion, yielding a value per share of about $47. At the end of June 10, when I completed my valuation, the stock price was close to $170, well above my estimated value. What the stock dropped almost $41 on June 11 to $127/share, it still remained over valued.

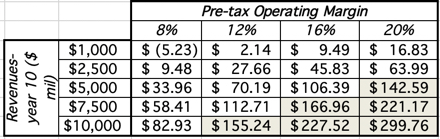

What if? As with any young company, the value of Beyond Meat is driven almost entirely by the story you tell about the company, and in this case, that story revolves around two key inputs. The first is the revenue that you believe the company can generate, once mature, and that reflects how big you think the market for meatless meats will get and Beyond Meat’s market share of the market. The second is its profitability at that point, which is a function of how much pricing power you believe the company will have. While I have assumed that Beyond Meat will deliver about $3 billion in revenues in 2028, with an operating margin of 13.22%, your story for the company can lead you to very different estimates for one or both numbers:

The shaded cells represent break even points, where you could justify buying Beyond Meat at the price ($127) it was trading at on June 11, 2019. Put differently, if your story for the meatless meat market and Beyond Meat’s place in it leads you to revenues of $5 billion or higher with an operating margin of 20%, you should be a value investor in the company.

Macro Bets and Micro Value

As you can see from the what-if analysis on Beyond Meat’s value, the value that you obtain for Beyond Meat is determined mostly by how large you believe that market for meatless meats will end up being. In fact, there are some investors whose primary reason for investing in Beyond Meat is as a bet on a macro trend towards vegan and vegetarian diets. That said, it is worth remembering that investors don’t get pay offs from making the right macro bets, but from the micro vehicles (individual investments) that they use as proxies for those bets. To get the pay off from a correct macro call, there are two additional assessments that investors have to make:

- Industry structure: A growing market may not translate into high value businesses, if it is crowded and intensely competitive. That market will deliver high revenue growth, but with low or no profitability, and no pathway to sustainable profits and value added. In contrast, a growing market where there are significant barriers to entry and a few big winners can result in high-value companies with large market share and unscalable moats.

- Winners and Losers: Assuming that there is potential for value creation in a market, investors have to pick the companies that are most likely to win in that market. That is difficult to do, when you are looking at young companies in a young market, but there is no way around making that judgment. In a post from 2015, I argued that in big (or potentially big) markets, you can expect companies to be collectively over valued early in the game.

In my Beyond Meat Inc (NASDAQ: BYND) valuation, I have implicitly made assumptions about both these components, by first allowing operating margins to converge on those of large food processing companies and then making Beyond Meat one of the winners in the meatless meat market, by giving it a 25% market share. My defense of these assumptions is simple. I believe that the meatless meat market will evolve like the broader food business, with a few big players dominating, with similar competitive advantages including brand name, economies of scale and access to distribution systems.

I also believe that Beyond Meat and Impossible Foods, as front runners in this market, will use their access to capital to scale up quickly. Their use of fast food chains feeds into this strategy, with bulk sales increasing revenues quickly, allowing for economies of scale, and name-brand offerings (Impossible Whopper at Burger Kind, Beyond Famous Star burger at Carl’s Jr.) helping improve brand name recognition. I will undoubtedly have to revisit these assumptions as the market evolves and some of you may disagree with me strongly on one or both assumptions. If so, please do download the spreadsheet and make your best judgments to derive your value for the company.