Investors love stocks that consistently beat the Street without getting ahead of their fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with robust and improving financial metrics that support strong price growth. Does Oracle Corporation (NASDAQ:ORCL) fit the bill? Let’s look at what its recent results tell us about its potential for future gains.

The graphs you’re about to see tell Oracle Corporation (NASDAQ:ORCL)’s story, and we’ll be grading the quality of that story in several ways:

- Growth: are profits, margins, and free cash flow all increasing?

- Valuation: is share price growing in line with earnings per share?

- Opportunities: is return on equity increasing while debt to equity declines?

- Dividends: are dividends consistently growing in a sustainable way?

What the numbers tell you

Now, let’s take a look at Oracle Corporation (NASDAQ:ORCL)’s key statistics:

ORCL Total Return Price data by YCharts.

| Criteria | 3-Year* Change | Grade |

|---|---|---|

| Revenue growth > 30% | 38.60% | Pass |

| Improving profit margin | 28.50% | Pass |

| Free cash flow growth > Net income growth | 60.6% vs. 78.1% | Fail |

| Improving EPS | 86.80% | Pass |

| Stock growth (+ 15%) < EPS growth | 41.7% vs. 86.8% | Pass |

Source: YCharts.

*Period begins at end of Q2 2010.

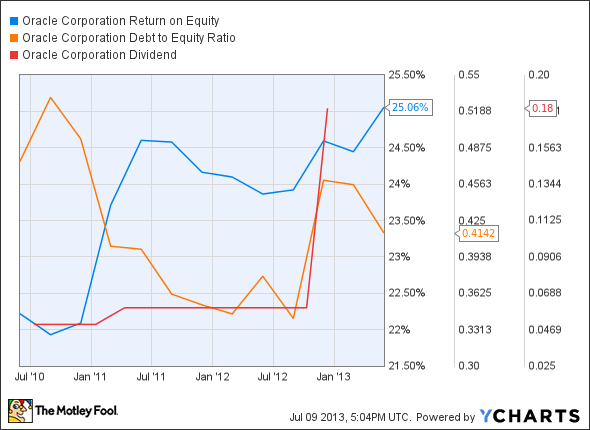

ORCL Return on Equity data by YCharts.

| Criteria | 3-Year* Change | Grade |

|---|---|---|

| Improving return on equity | 12.8% | Pass |

| Declining debt to equity | (13%) | Pass |

| Dividend growth > 25% | 260% | Pass |

| Free cash flow payout ratio < 50% | 10.8% | Pass |

Source: YCharts.

*Period begins at end of Q2 2010.

How we got here and where we’re going

Oracle Corporation (NASDAQ:ORCL) just about knocks it out of the park here, with eight out of nine possible passing grades, and it has a very good chance to gain a perfect score next time around. It lost out on a perfect score only because net income outpaced free cash flow during our tracked period — however, the raw numbers reveal that Oracle Corporation (NASDAQ:ORCL)’s free cash flow is more than $2 billion higher than its net income. That makes it an even more appealing value, as its price-to-free cash flow ratio is presently barely in double-digit territory. How could Oracle Corporation (NASDAQ:ORCL) push its revenue even higher over the next few quarters and gain that last elusive passing grade? Let’s dig a little deeper.

Investors’ biggest fear has been that the software giant has been (or is being) left behind by its peers when it comes to the cloud-computing revolution. Oracle has traditionally made its money by licensing software to businesses, and to a lesser extent, through hardware sales via its Sun Microsystems subsidiary. Neither has posted particularly strong growth for Oracle, as enterprises are turning to cloud software that allows employees to access company-critical data no matter where they work.

Last month, Oracle decided to use its hefty cash flow and powerful brand name to muscle its way into the sector. The software leader recently announced three cloud-computing partnerships that may allay investor fears. Perhaps the most intriguing of these partnerships is between Oracle and rival salesforce.com, inc. (NYSE:CRM). This could turn out to be quite lucrative for both companies, as Oracle gains a high-profile market for some of its second-tier products (such as the Exadata data management platform), and salesforce.com, inc. (NYSE:CRM) gets a very committed partner for its back-end operations.

Oracle’s also partnered with NetSuite Inc (NYSE:N) and Microsoft Corporation (NASDAQ:MSFT). The NetSuite partnership will see Oracle combine its human capital management software — which allows businesses to streamline human resources operations — with NetSuite Inc (NYSE:N)’s enterprise resource planning software, which businesses use to coordinate the management of information between a company and its stakeholders. These combined applications should be available by the end of this year. Oracle’s partnership with Microsoft, on the other hand, focuses primarily on its Java software suite, which it will license to Microsoft Corporation (NASDAQ:MSFT) for use in its existing cloud-based services in conjunction with Oracle’s other software tools.

Oracle also recently announced the purchase of up to $12 billion of its own shares. Another big investor-side boost involves the doubling of its dividend. Despite that payout bump, Oracle is still scheduled to pay out only 17% of its projected 2014 EPS (and less in free cash flow terms), leaving the company plenty of room to raise its dividend again without taking away precious cash flow required to boost its all-important research spending.

Putting the pieces together

Today, Oracle has many of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy — or to stay away from a stock that’s going nowhere.

The article Is Oracle Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes has no position in any stocks mentioned. The Motley Fool recommends Netsuite and salesforce.com and owns shares of Microsoft and Oracle.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.