This guest post has been written by Mike McNeil, passionate investor, founder of Dividend Stocks Rock and author of The Dividend Guy Blog.

The current bull market hides many companies’ flaws. In fact, since 2009, almost all stocks have gone up one way or another. My 11-year-old boy could probably do as well as most investors on the Street. This situation makes it even more difficult for investors to differentiate the good picks from the bad seeds.

Nonwarit/Shutterstock.com

For example, when you look at the Honeywell International Inc. (NYSE:HON) and General Electric Company (NYSE:GE) stock price graph for the past 5 years, both seem to be a good investment:

Source: YCharts

While Honeywell International Inc. (NYSE:HON) clearly outperformed General Electric during this period, most GE shareholders won’t complain about its performance. I know that General Electric is a very popular stock among investors. The company has been around for over 100 years, and has performed quite well for decades. However, I believe the current bull market is hiding many flaws, and Honeywell is a better option for those who are looking to add an industrial stock to their portfolio. Ironically, Honeywell failed to merge with General Electric back in 2001.

As a dividend growth investor, my focus when analyzing companies is payouts and potential increases. In order to do so, I have studied 3 components leading to sustainable payment increases as per the 7 dividend growth investing principles:

– Revenue trend

– Earnings trend

– Dividend and payout ratio trend

I will compare both companies using those metrics, and conclude my analysis with a valuation of both stock prices.

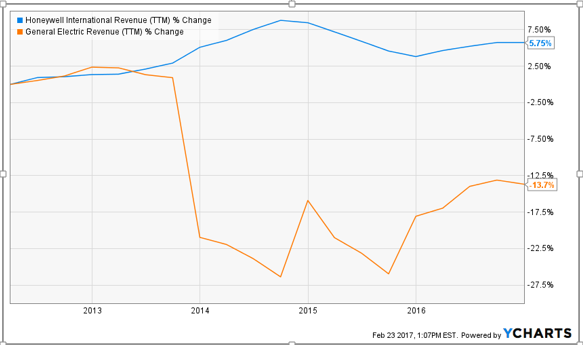

Revenue

Source: YCharts

While Honeywell’s revenue growth over the past 5 years is far from being spectacular, General Electric is having several problems generating growth. This is obviously caused by the sale of GE Capital, a lucrative but highly volatile segment. The most recent bump in 2016 results is due to the acquisition of Alstom. Over the past few years, General Electric has focused on restructuring their “GE Store”:

Source: GE China Investor Forum Presentation

Follow Honeywell International Inc (NYSE:-)

Follow Honeywell International Inc (NYSE:-)

In contrast, Honeywell has put additional focus on software engineering, with nearly 11,000 engineers working on software instead of more classic industrial goods. The software business is better, as it enables more combinations of services and drives higher margins. Honeywell certainly has some solid growth potential for future investing.

Source: Honeywell Q4 2016 Presentation.

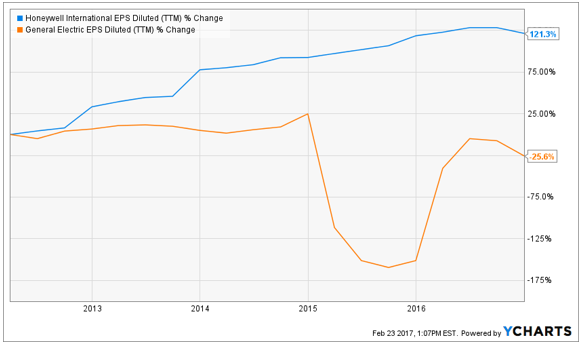

Earnings

Source: YCharts

When looking at revenue perspectives, we can see both companies will not burst expectations with soaring numbers in upcoming years. However, when looking at earnings, we can clearly see that Honeywell International Inc. (NYSE:HON) is exhibiting success improving their earnings compared to General Electric. Honeywell International Inc. (NYSE:HON) management expects to grow EPS by 6% to 10% while GE expects growth of 3% to 5%.

General Electric Company (NYSE:GE) will have a hard time replacing GE Capital’s profit potential through core industrial segments. Additionally, its Alstom integration has proven less profitable than expected so far due to speed bumps during the integration process.

Honeywell’s strong position in the aerospace industry, and safety products will help the company benefit from an aircraft upcycle. Did you know that HON won 100% of the jet propulsion engine competitions for medium-to-large business jets since 2001? That’s a very good batting average!

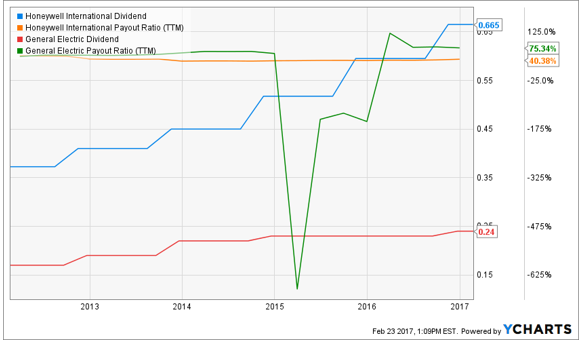

Dividend Perspective

Source: YCharts

GE’s current payout ratio seems under control with a 75% ratio. However, when we use the cash payout ratio, we can see the company is bleeding cash at the moment (the ratio is at -327%).

Remember, the payout ratio is a reliable indicator of a company’s ability to sustain its dividend, but it remains based on accounting numbers, not real cash. Even then, with slow revenue and earnings growth, a 75% payout ratio doesn’t give you much room for growth.

Honeywell International Inc. (NYSE:HON)’s management announced last year that its dividend payout ratio will increase in the upcoming 4 years. They were able to keep it around 40% for the past 5 years, but now feel it’s the time to reward investors. The dividend payment increase was of 15% and 11.76% in 2016. I’m not putting on my rose-colored glasses, and expecting a 12% dividend growth in the next 10 years, I can appreciate the growth will be significant for several years to come. In comparison, Honeywell clearly has more room than GE to boost their payouts in the upcoming years.

Valuation

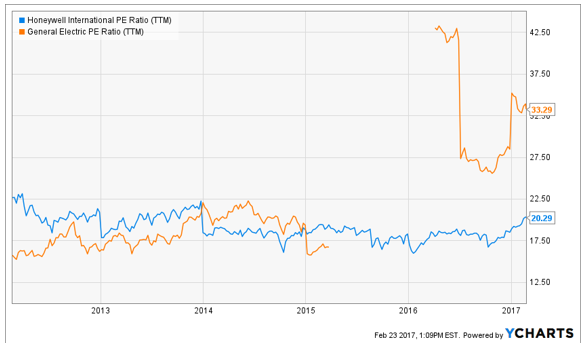

When it comes to valuation, I use 2 different techniques. The first one will give me a good idea of what the market value of the company is. I use the historical P/E ratio:

Source: YCharts

Both companies used to trade at about the same valuation for 3 years in a row until General Electric Company (NYSE:GE) posted losses. Now that the company is “back on track”, it seems their stock price is living on “investors hope” that it will get better. On the other hand, Honeywell (HON) trading at a P/E of 20 doesn’t look like an incredible deal either.

I’d like to go deeper in my analysis, and use a double stage dividend discount model (DDM) to determine the company’s value.

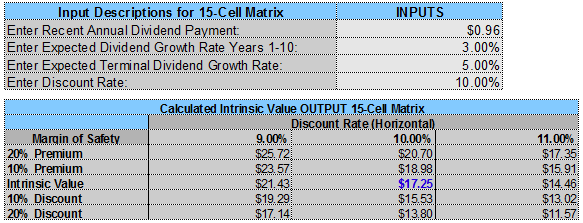

GE’s DDM calculations:

Source: Dividend Monk Toolkit Calculation Spreadsheet

I’ve used a discount rate of 10% as I still see various risks attached to GE’s performance in the upcoming years. They recently reported losses in 2015 and 2016, they show difficulty integrating and generating synergy from their Alstom acquisition, and they struggle to identify growth vectors in the future.

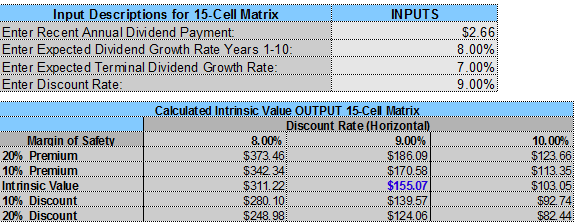

Honeywell International Inc. (NYSE:HON)’s DDM calculation:

Source: Dividend Monk Toolkit Calculation Spreadsheet

As you can see, I’ve been a lot more generous with my Honeywell International Inc. (NYSE:HON) valuation. This is because the company has increased its EPS strongly in the past 5 years and continues to aim at high single-digit growth. Management has already announced that their payout ratio will rise in the upcoming years, leading to an aggressive dividend growth rate. Finally, I’ve used a 9% discount rate, as I judge Honeywell’s fundamentals as being stronger and less volatile than General Electric’s.

Final Thoughts

I know Honeywell International Inc. (NYSE:HON)’s dividend yield is a lot less attractive than GE’s right now. However, future payout growth should invite additional investors to consider Honeywell over General Electric. In the future, and based on historic performance, it has been clear to me that Honeywell will continue to outperform General Electric Company (NYSE:GE).

Follow General Electric Co (NYSE:GE)

Follow General Electric Co (NYSE:GE)

Disclaimer: I own shares of HON in my Dividend Stocks Rock portfolios.