The most fundamental way in which to value a stock is by performing a discounted cash flow calculation, or DCF. If you’re a regular reader of articles about stocks you’ve likely seen this method used countless times. DCF calculations are ultra-sensitive to the inputs, meaning that a small change in a parameter can lead to a dramatic change in the result. This is dangerous if you blindly trust a calculation, as many seem to do. It’s important to understand exactly what can go wrong.

A quick overview

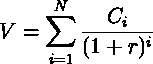

The value of a company is the sum of all future cash flows discounted back to today by a discount rate, plus or minus any net cash or net debt. Imagine a company which makes $1 million in profit every year and expects to continue to do so into the foreseeable future. If we use a discount rate of 10% then next year’s profit is worth about $909 thousand today, the profit in the year after that is worth $826 thousand, and so on. Adding this all up we arrive at a company value of $10 million.

This makes sense, since if we bought the company for $10 million today the profit would give us a 10% return on our investment, exactly our discount rate. The discount rate, then, is your required rate of return. If I had used a 12% discount rate in the example above then the value of the company would have been only $8.33 million. An 8% discount rate would have led to a $12.5 million valuation.

When you value a stock the process is exactly the same, except the profits are typically expected to grow over time. In general, the formula for a DCF calculation is:

where r is the discount rate, C is the cash flow in each year, and i is the year. In the example above, with a constant profit, C would always be the same.

I’ll use two different stocks to point out the potential problems with DCF calculations, Facebook Inc (NASDAQ:FB) and Tesla Motors Inc (NASDAQ:TSLA).

Problem 1: The discount rate

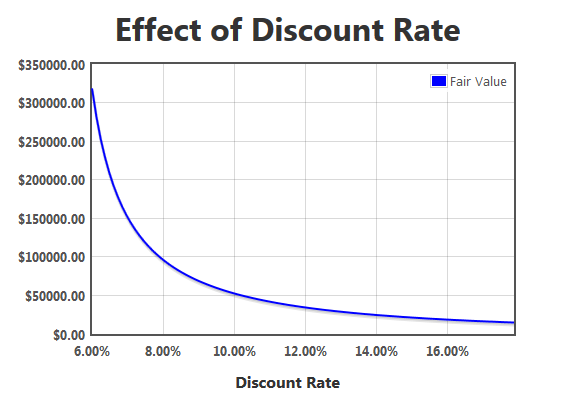

Facebook Inc (NASDAQ:FB) recorded a free cash flow of $377 million in 2012, and for the sake of simplicity I’ll use this value in my calculation. Let’s assume that the free cash flow grows by 30% annually for the next 10 years and by 5% annually after that. Whether this assumption is reasonable or not doesn’t really matter, because what I’m interested in is how the choice of the discount rate changes the value of the company.

If you use a discount rate of 10% you arrive at a fair value of about $52 billion, not too far off from the current market capitalization. If you bump that up to 15%, a value which I like to use, the fair value plummets to just $21 billion.

Here’s where it gets dangerous. I’ve seen people use discount rates around 7% when dealing with companies like Facebook Inc (NASDAQ:FB). This would lead to a fair value of $150 billion! That’s a factor of 7 higher than the value with a 15% discount rate.

Which discount rate is correct? None of them are. The discount rate is your required rate of return, and that varies from person to person. I like to use both 12% and 15% to get a nice fair value range, implying that I want my rate of return to be between these values. Using a 7% discount rate assumes that you only want a 7% return, in which case you should just go buy an broad-market ETF and not think about individual stocks anymore.

The bottom line about discount rates is this: small changes in the discount rate lead to big changes in the fair value. Too low of a discount rate will give you an unrealistically high result.

Problem 2: Growth rate is too close to the discount rate

I’ll stick with Facebook Inc (NASDAQ:FB) to demonstrate the second problem. Let’s do the same calculation as above, using a 7% discount rate, but instead of a 5% long term growth rate after 10 years let’s bump that number up to 6.5%. Surely this slight increase can’t have too big of an effect on the value of the company.

Well, it does. The fair value nearly quadruples to $575 billion. A long-term growth rate of 6.9% values Facebook Inc (NASDAQ:FB) at $2.8 trillion! How can such a small change lead to such outrageous values? Because the growth rate is too close to the discount rate. The fair value goes to infinity at a long-term growth rate equal to the discount rate, so any where close to that leads to huge values.

This is why you simply can’t assume that the cash flow will grow at 20% per year forever – you’d get a nonsense answer. The typical solution is choosing a fairly low long-term growth rate, say 3%, and admit that you have no idea what is actually going to happen ten years from now anyway. This brings the answers back into reality.

Problem 3: Overly optimistic growth rate

Now let’s turn to Tesla Motors Inc (NASDAQ:TSLA). Is it possible to justify Tesla’s crazy-high P/E ratio by tweaking parameters in a DCF calculation? Well, that’s likely what analysts with their price targets do every day. Tesla Motors Inc (NASDAQ:TSLA) recently had its first quarter of profitability after burning through cash for many years. The company is valued at $12.5 billion.

Let’s say that next year Tesla manages $50 million in profit. For the next 20 years the company grows at a high rate and then by 5% annually after that. Using a discount rate of 7% this high growth rate needs to be about 18% to fairly value the stock at the current market price.

I don’t know how fast Tesla Motors Inc (NASDAQ:TSLA) will grow 12 years from now. No one does. In order to justify the current valuation you have to make some pretty bold assumptions. And because the calculation is so sensitive to those assumptions the answer has little meaning at all. If the growth rate is dropped to 15% instead of 18% the value of the company falls by nearly 40%. If you’re wrong by 3% the company goes from being fairly valued to being outrageously overvalued.

The fact that you can tweak the parameters slightly and obtain a completely different result should tell you that the result doesn’t carry much meaning. When an analyst comes out with a price target this is exactly what they do. They tweak things until the answer comes out “right”.

A fuzzy future

Both Facebook Inc (NASDAQ:FB) and Tesla Motors Inc (NASDAQ:TSLA) pose a problem for investors – the future of both companies is unpredictable. Facebook is still trying to figure out how to monetize its enormous user base, and with young people increasingly ditching the site for alternatives like Twitter the company may have trouble growing its user base going forward. Is it possible for Facebook to grow its earnings by 30% per year? Sure. Do I have any confidence at all that the company will actually achieve this? Absolutely not. This is why doing a DCF calculation for Facebook Inc (NASDAQ:FB) is almost useless.

I don’t know what Facebook will look like as a company 10 years from now, so why would I invest in it? Will its profits come mainly from advertising, or will the company transform into something else entirely? Will users stick with Facebook, or will an alternative draw people away? These questions make valuing Facebook Inc (NASDAQ:FB) very difficult.

Tesla Motors Inc (NASDAQ:TSLA) has the same type of problem. The electric car market right now is tiny, but once it reaches a critical mass there will be a lot more competition than there is today. Is there anything truly unique about Tesla which suggests that the company will become a major car maker 20 years from now? Not really. The auto industry is extremely capital intensive and Tesla will struggle to scale up its operations as the market grows. If the company ever manages to produce a mainstream car it will likely face a slew of lower-cost competition from the the major auto companies. I don’t think Tesla will be meaningfully profitable for quite some time, and the growth necessary to justify its current valuation is just not realistic.

There is a chance, however slight, that Tesla Motors Inc (NASDAQ:TSLA) grows into a behemoth which dominates the electric car market. But the price you’re paying for the shares today seems to assume that this is a foregone conclusion instead of a low-probability outcome. The odds are not in the favor of the Tesla investor.

The bottom line

The biggest danger with a DCF calculation is trusting the results too much. Many people have an opinion going into it and then tweak the parameters so that the answer matches that opinion. Whenever someone claims that a stock is worth some amount based on a discounted cash flow calculation, make sure that the inputs make sense. If they don’t, then the “value” calculated is meaningless. Garbage in, garbage out.

The article Be Careful With Discounted Cash Flows originally appeared on Fool.com and is written by Timothy Green.

Timothy Green has no position in any stocks mentioned. The Motley Fool recommends Facebook and Tesla Motors (NASDAQ:TSLA) . The Motley Fool owns shares of Facebook and Tesla Motors. Timothy is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.