![]()

On April 25, the company reported first-quarter financial results. Compared to the same quarter in 2012, net income increased 5.29%, from $9.45 billion ($2 per share) to $9.5 billion ($2.12 per share). However, the disappointment that stemmed from the report was a result of total revenue falling 12.29% year over year. Wall Street sent the stock tumbling downward the next day.

The company possesses a TTM profit margin of 9.62%, which is anticipated to fall to the 8% mark by 2017. Based on market capitalization, the company is the second most valuable in the world at $403.33 billion. At current prices, the company pays out a dividend yielding 2.80%.

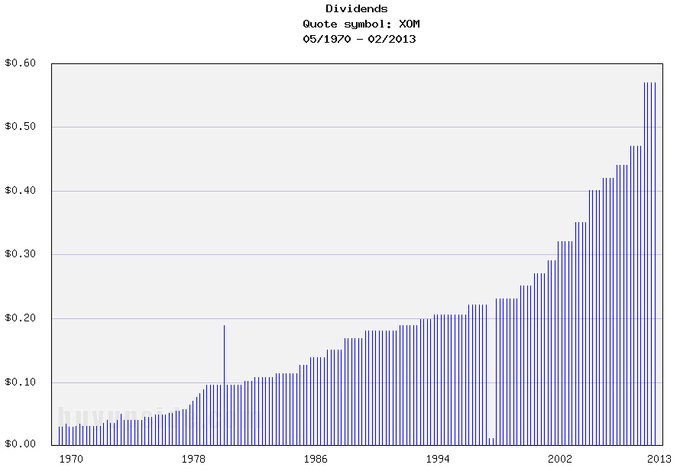

This energy giant recently announced an increase in its quarterly dividend payout, from $0.57 to $0.63, representing the 31st consecutive annual dividend increase by the company.

As Exxon nears all-time highs, is Exxon a solid long-term investment or should investors look elsewhere for black gold? Let’s try and find out.

Strengths:

Solid revenue growth:

In 2003, Exxon Mobil Corporation (NYSE:XOM) reported revenue of $246.74 billion; in 2012, the company announced revenue of $482.29 billion, representing year over year annual growth of 6.93%, a trend that it is highly anticipated to sustain into the future with projections placing 2019 revenue at $715 billion (this growth has been a result of consistent reinvestment by the company).

Dividend:

Currently, the company pays out quarterly dividends of $0.63, which annualized puts the dividend as yielding 2.80%, a major advantage for long-term investors.

Basement valuation:

At the moment, Exxon Mobil Corporation (NYSE:XOM) carries a price earnings ratio of 9.29, a price to sales ratio of 0.86, and a price to book ratio of 2.44; all of which indicate a company trading with a basement valuation.

Relatively low volatility:

Presently, the company has a beta of 0.50, representing a company trading with considerably less volatility than the overall market, a major advantage for long-term investors.

Cash flow position:

In 2011, Exxon generated $56.66 billion in cash flow, up from $30 billion in 2003, and this cash flow position is extremely important as it gives the company the financial security to reward shareholders.

Institutional vote of confidence:

46.25% of shares outstanding are held by institutional investors, equating to nearly $200 billion, displaying the confidence some of largest investors in the world have in the company and its future.

Broad diversification of business:

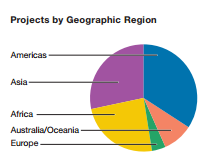

Exxon Mobil Corporation (NYSE:XOM)’s business is spread across the world, with no one region making up more than roughly 33% of overall business, and with this broad diversification comes a greater level of predictability and security for investors.

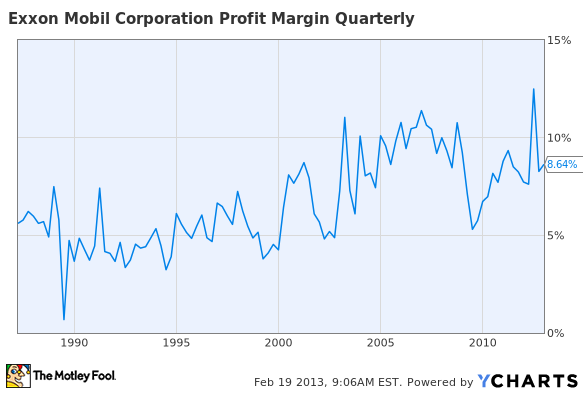

Long-term trend of margin expansion:

In 1990, the company’s profit margin was sitting around 5%, which has expanded to the current 8.64% level, and this trend of long-term margin expansion is a major strength.