Dynex Capital Inc (NYSE:DX) is operating as a mortgage REIT since 1988 with an objective of providing higher risk-adjusted returns to its shareholders primarily through dividends. For this purpose, the company originates and securitizes various types of loans, largely single-family and commercial mortgage loans and manufactured housing loans. Besides, the company invests in Agency and non-Agency mortgage backed securities. The company’s Agency RMBS consist of hybrid adjustable and ARMs. The primary source of company’s income is net interest spread, which is the spread over what the company earns on its interest yielding assets and what it pays on its interest bearing liabilities.

At the end of the fourth quarter, the company had an investment portfolio of $4.18 billion, compared to $4.3 billion at the end of the linked quarter. The following graphs will display each security type in the company’s investment portfolio.

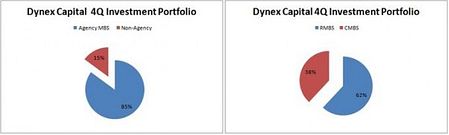

It is evident from the above graph that Dynex Capital has a large concentration of Agency MBS in its investment portfolio. At the end of the most recent quarter, Agency MBS were 85% of the entire portfolio, while non-Agency MBS were 15%. However, during the quarter the company declined its Agency holdings by 229 million, primarily through prepayments and amortization of premiums. During the recent quarter, RMBS and CMBS were $2.6 billion (62% of the portfolio) and $1.6 billion (38% of the portfolio), respectively.

Recent Quarter’s Performance

Dynex Capital reported strong fourth quarter results on February 20, 2013. The results were positively affected by higher interest income, higher gain on sale of investments, partially offset by higher interest expense and higher general and administrative expenses during the quarter.

At the end of the fourth quarter, the company generated of $31.6 million, up 33.2% from a year ago. This improvement in interest income was a result of higher interest income from both Agency and non-Agency MBS, partially offset by securitized mortgage loans. Higher interest income was attributed to higher interest yielding assets, partially offset by lower net interest spread. While interest yielding assets of $4.12 billion were up 10.5%, during the quarter, of 1.93% was recognized, down 7 basis points from a year ago.

during the most recent quarter was $10.4 million, up 55% compared to the same quarter of the previous year. The surge in interest expense was primarily due to the rise in repurchase agreement costs, partially offset by non-recourse collateralized financing.

As a result, the company posted a of $21.2 million, up 25% year over year, on higher interest income. The bottom line for the fourth quarter was also supported by lower and higher . The company recognized $22,000 in provision for loan losses during the most recent quarter, compared to $121,000 a year ago. $2.04 billion were recognized as gain on sale of investments, compared to $773,000 a year ago. climbed 8% year over year, on higher compensation and benefits, partially offset by lower other general and administrative expenses.

As a result, Dynex was able to post a of $19.6 million, compared to $14.4 million a year ago.

Other Key Matrices of Dynex Capital

At the end of the fourth quarter, Dynex Capital posted a book value of $10.3, slightly down from $10.31 a year ago. The prepayment speed for Dynex Capital’s investment portfolio was up from 18.7% to 19% over the same time period, while the leverage came down from 6.1 times to 5.9 times.

Competition

Dynex Capital competes with other hybrid mortgage REITs in the United States, like Two Harbors Investment Corp (NYSE:TWO) and CYS Investments Inc (NYSE:CYS).

Two Harbors, formed in 2009, owns a highly well diversified investment portfolio with 81% Agency RMBS and the remaining non-Agency RMBS. Besides, the company diversifies its portfolio with the combination of fixed rate and adjustable rate securities. Fixed rate are 80% of the recent quarter end investment portfolio. Just like Dynex, Two Harbors posted 2.9% net interest spread, down from 3.1% in the linked quarter, while its leverage came down from 3.8 times to 3.4 times.

CYS Investments Inc (NYSE:CYS), a similar hybrid mortgage REIT, owns an investment portfolio consisting of 56% 15-year fixed rate MBS, followed by .19% hybrid ARMs and 18% 30-year fixed rate securities. The company reported a net interest spread of 0.94%, down 30 basis points from the linked quarter. Its prepayment speed at the end of the fourth quarter was up 3 basis points to 17.6%, while the book value decreased 8% compared to the linked quarter.

In contrast, American Capital Agency Corp. (NASDAQ:AGNC) and Annaly Capital Management, Inc. (NYSE:NLY) invest exclusively in Agency mortgage backed securities. American Capital’s recent earnings were positively impacted by a hike in asset yields, supported by a hike in the interest yielding assets during the quarter. Asset yields increased despite the challenging micro-environment, where the Fed is committed to keep the rates low and the yield curve flat. American Capital is believed to be a highly prepayment protected portfolio. Annaly Capital’s asset yields and net interest spread were compressed again during the most recent quarter. However, the management managed expenses well during the fourth quarter, which is why they declined 36%. Annaly is involved aggressively in diversifying its portfolio by acquiring CreXus Investments.

Future Outlook

2013 will be marred by low interest rate for the US mortgage RIETs as the Fed has dispelled any concerns regarding the risk of its aggressive bond buying and the resultant halt of the strategy. Ben Bernanke has again shown his resolve to continue the bond buying program to stimulate the US economy. This means, the downward pressure on bond yields will continue to prevail, which will continue to decrease the asset yields earned by mortgage REITs. The lowered asset yields result in lower net interest rate spread and resultantly lower dividend distributions. Give the situation, I believe Hybrid REITs with well diversified MBS portfolio will be the best choice in the coming quarters, as their high yielding assets other than Agency RMBS will continue to support the bottom line and the net interest rate spreads. Since Dynex Capital is both hybrid and possesses a very well diversified MBS portfolio, it will be one of my top picks within the mortgage REITs sector for 2013.

Investment Strategy

I am bullish on Dynex Capital due to its highly diversified MBS mix, particularly given the continued Fed bond buying. The company offers a dividend yield of 11.2% and an upside potential of 5.3% on my target price of $10.95. The large presence of high yielding non-Agency MBS in the company’s highly diversified MBS mix will enable it to maintain its current dividend throughout 2013. It is also worth noting that Dynex Capital increased its quarterly dividend in 2012 when most of its peers were forced to cut their shareholder distributions.

The article This 11% Yielder Is Well Positioned to Maintain Its Dividend originally appeared on Fool.com and is written by Adnan Khan.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.