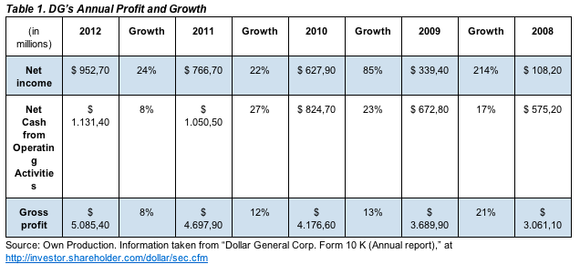

When thinking about discount retailers in the United States, Dollar General Corp. (NYSE:DG) is as big as it gets. With over 10,000 stores located in 40 states, it has shown a consistent growth in sales for 23 years now. Here is a chart that shows how strong Dollar General Corp. (NYSE:DG) has grown in the past years:

In addition, Dollar General Corp. (NYSE:DG)‘s management has been focused on store growth:

The constant progress of the company shows certain independence from the fluctuations of the economy and overall prices. However, as attractive and safe as investing in this business may seem, their Annual report warns those interested about several risks. We will focus on three main ones:

1) Intense competition in the retail market

Dollar General Corp. (NYSE:DG) competes with different retailers like Family Dollar Stores, Inc. (NYSE:FDO), Dollar Tree, Inc. (NASDAQ:DLTR), Wal-Mart Stores, Inc. (NYSE:WMT), Walgreen Company (NYSE:WAG) and CVS Caremark Corporation (NYSE:CVS), amongst others. Although some of these companies face overexpansion issues and diminishing returns, others still have greater financial, logistic and operational resources than Dollar General Corp. (NYSE:DG), thus being able to attain better deals with suppliers. In order to maintain competitiveness, prices at Dollar General Corp. (NYSE:DG)‘s stores must remain low, therefore reducing a potential increase in profit margin.

Another source of concern is the incursion of large format stores in the “small box” field, which is highlighted by many as the main Dollar General differential. Due to dollar stores’ high performance over the past years, Wal-Mart Stores, Inc. (NYSE:WMT) has started to target Dollar General stores by opening small Neighborhood Markets and Express stores and offering “price comparison” policies (that aim to offer lower prices than its competitors).

Competitiveness could also be highly affected by government decisions.

Dollar General’s performance is vastly influenced by the payroll tax cut implemented in 2011 and the distribution of food stamps

(which represent around 5% of the stores’ sales). Cuts and set-backs in these policies would importantly impact the company’s profit.

2) Substantial debt to be repaid or refinanced (variable rate and restrictions apply)

Dollar General´s 10K states:

“

We have substantial debt that must be repaid or refinanced at or prior to applicable maturity dates which could adversely affect our ability to raise additional capital to fund our operations and limit our ability to pursue our growth strategy or other opportunities or to react to changes in the economy or our industry.”

This outstanding debt, of over U$S 2700 billion (by February 2013), implies important risks related to limitations in the use and flow of cash: many resources that could and should be used to gain competitiveness and adapt to new market imperatives, could be allocated to the payment of debt, especially if Dollar General fails to refinance a significant part of it.

As compared to its main competitors, Dollar General has the biggest debt if contrasted to its capital or equity level:

Besides the inherent restrictions imposed by debt obligations, Dollar General’s loan agreements comprehend other specific limitations (i.e. inability to acquire new debt, sell assets, issue disqualified stock, etc) that widely reduce the company’s decision margin.

In addition to the previously mentioned issues, the corporation must face variable interest rates. This means that the actual debt figure is somewhat unpredictable and largely subject to fluctuations in the US and World economy.

3) Limits on operating margin upside

Dollar General Corp (NYSE:DG). has shown to be very successful in the expansion of operating margins, increasing its figures from the 7% span to a current 10%. This has meant that around a 40% of the company’s profits over the last five years has accounted for these margins. Unfortunately (for the investors, at least), this tendency seems to be reaching its limit. Credit Suisse (See Credit Suisse, “Dollar Stores, Assuming Coverage. Multi-year Run…” pp. 44 and 45

points out four main reasons to believe this:

–

Growth shifting to lower margin urban markets

–

Management’s focus on unit growth (delaying price increases) in a re-inflationary environment

–

Increased mix pressure from the additional expansion into low margin categories like Tobacco

–

Increased competitive pressure from Wal-Mart

Foolish conclusion

In conclusion, Dollar General’s financial performance largely depends on the company’s ability to manage and respond effectively to the above mentioned challenges presented by the main competitors and the general increase in market competition, as well as its capability to cope with new government (mainly fiscal) or creditor imposed situations.

The article 3 Risk Factors That Dollar General Investors Should Evaluate originally appeared on Fool.com is written by Victor Selva.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.