Textbooks will tell you that economies work in concert with some kind of ideal and consistent. Unfortunately, it never quite works out like that. In the financial sector in particular we have seen some unusual developments in recent years.

On a historical basis the sector looks cheap, with many of the leading companies trading at below book value; however, we are living in uncertain times and the credit cycle is not the same as it once was. So do the financial companies present good value right now?

It’s different this time

These are some of the most famous last words in investing. They induce investors into making assumptions that they build into stocks, which then promptly disappoint them. In the case of the financials we are seeing ongoing weak consumer demand for loans; however, I think it would be a mistake to assume that it really is different this time. At some point–as long as the economy keeps improving–consumer demand for loans will increase. History suggests that when employment and incomes increases then loan growth will follow.

With this said it is worth reflecting on how slow the recovery has been. Employment gains have been on a par with previous recoveries, but nothing near enough to recompense for jobs lost in the recession. Moreover, we have come through a few years of consumers deleveraging, and such behavior can become habitual. Meanwhile, the Federal Reserve is doing anything it can to throw liquidity into the economy. Interest rates are low and financials are facing declining net interest margins as they struggle to replace higher rate loans that are maturing. A veritable mix of pluses and minuses.

How this plays out in the Industry

We can see these issues playing out in the metrics of the lenders. For example, here is Discover Financial Services (NYSE:DFS)’ net charge off rate and delinquency rates for its US credit loans.

Clearly asset quality has improved in a rather dramatic way since the last recession, and it is notably lower than before.

While asset quality has improved across the board, low interest rates have created net interest margin (NIM) difficulties. For example, here is a look at Wells Fargo & Co (NYSE:WFC)’s NIM numbers.

In the case of Wells Fargo & Co (NYSE:WFC) It has seen significant increases in deposits, which created pressure on its NIM while new mortgage origination hasn’t been as strong as many might have hoped.

In a sense the whole industry is positioned in a similar manner. Asset quality is improving, but consumer demand remains weak and many loans are maturing, leading to significant amounts of runoff and capital appreciation.

Enter Capital One Financial Corp. (NYSE:COF)

Within financials the stocks that I like are Wells Fargo & Co (NYSE:WFC) (on the basis of its exposure to the US housing market and conservative approach), Goldman Sachs Group, Inc. (NYSE:GS) because it still trades below book value and offers significant upside from exposure to more M&A activity this year, and Capital One Financial Corp. (NYSE:COF).

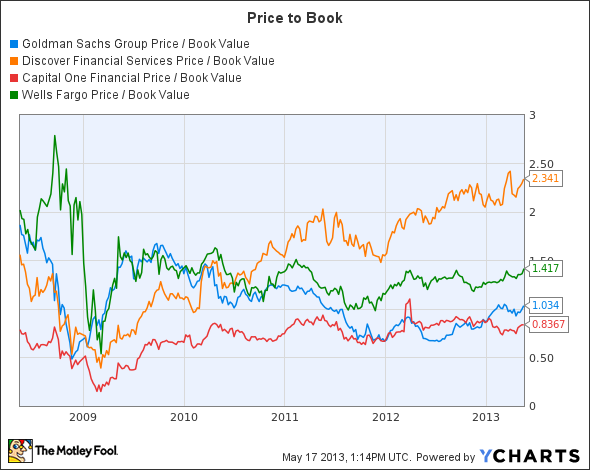

Here are the price to book numbers for the stocks discussed in this post.

GS Price / Book Value data by YCharts

Discover Financial Services (NYSE:DFS)’s evaluation reflects its more aggressive approach to lending, while Goldman Sachs Group, Inc. (NYSE:GS) remains subject to regulatory risk. Nonetheless I think Goldman is good value. I’m not the biggest fan of this company and the way that successive administrations have catered to its interests, but I’m willing to bet that these trends will continue and regulatory fears will ease. As for Discover Financial Services (NYSE:DFS), investors have to ask themselves if it is chasing too much business.