Dell Inc. (NASDAQ:DELL) had difficulty with beating earnings estimates this past quarter. The company was able to beat analyst estimate for revenues but missed on earnings. In an environment of declining PC sales, the company was able to off-set this decline with growth in revenue from its service segments.

The company reported a 5% decline in revenues from its products division (desktop computers, laptops, tablets, printers, and anything else hardware related). The company, on the other hand, reported a 6% growth rate in revenues from its services segment. The total revenue declined by 2% in the most recent quarter which was driven by falling computer demand.

The company reported a 73% decline in operating income with an 81% decline in year-over-year earnings per share. The decline in operating income and earnings is two-fold. First the company reported a decline in sales. But following that the company also reported that the cost of running the business increased by 12%. The increase in costs led to ultra-thin profit margins of 1.2% for the first quarter of 2013.

What to expect from Dell going forward

There has been an on-going debate over whether or not Michael Dell can pull-off a leveraged buy-out of his own company for $13.65 per share. The likelihood of that deal passing is slim as institutional investors like Southeastern Asset Management Inc believe that the stock is worth substantially more than $13.65 per share. Southeastern Asset Management Inc believes that Dell Inc. (NASDAQ:DELL)’s valuation should be at around $23.72 per share.

Now, I’m not saying Southeastern Asset Management is wrong, but the valuation seems a little rich. A full break-down of the valuation analysis can be found on its website. Upon close examination, Southeastern Asset Management is making a very good point. It’s getting ripped off, which is why Southeastern Asset Management Inc is proposing for Dell to offer a $12 special dividend to shareholders while keeping the stock publicly traded (I’ll have a full article written on this later on today).

After looking over the Southeastern Asset Management’s analysis of the financial valuation of the company. It is highly unlikely that Michael Dell will get away with buying the company out at $13.65 per share. However, the alternative deal proposed by Southeastern Asset Management is likely to keep investors on the fence up until the August 2nd shareholder meeting.

What’s going on in the desktop and laptop space?

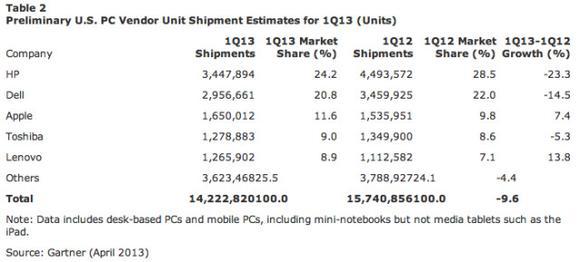

The decline in desktop shipments wasn’t completely due to the decline in demand for computers. When closely examining the figure below we can come up with an idea as to what actually happened.

Looking closely at the data it seems that Lenovo and Apple Inc. (NASDAQ:AAPL) were able to gain both in terms of market share and growth. Meanwhile, Hewlett Packard and Dell reported declines from their desktop and laptop divisions. Investors are hoping that the Windows 8 will be able to off-set some of the decline in desktop shipment sales as consumers adopt new products.

Believe it or not, I took on the challenge of visiting a Best Buy Co., Inc. (NYSE:BBY). When going into Best Buy, I was dismayed by a couple things about the Windows Operating System that the Geek Squad technician briefed me on. First Microsoft Corporation (NASDAQ:MSFT) didn’t implement a feature that would allow users to transfer programs from Windows 7 onto Windows 8. In fact, programs aren’t transferrable between the two operating systems. This means that users would have to purchase another copy of the software. In order to counter this negative effect, software developers like Adobe Systems Incorporated (NASDAQ:ADBE) is offering its Creative Cloud through a subscription rather than selling the product through a perpetual license. This allows users to upgrade from Windows 7 to Windows 8 without worrying about purchasing another software program.

More and more software companies are likely to adopt a subscription based approach in order to maximize revenues and make it easier for users to upgrade computers.

Apple dominates cloud

Apple Inc. (NASDAQ:AAPL) remains a compelling investment opportunity as it was able to increase sales for its Apple desktop and laptop products. Apple allows users to store data and programs through its Apple ID making it easier for users to transfer files and programs between all of the user’s Apple devices. This allows for faster adoption of Apple products and makes it easier for users to upgrade. It also helps that Apple Inc. (NASDAQ:AAPL)offers customer support through its genius bar at Apple store locations across the United States.

Apple Inc. (NASDAQ:AAPL) is pulling ahead in market share while Microsoft is hounding Apple Inc. (NASDAQ:AAPL) with Windows 8 mobile. In the mobile wars, Apple is certainly far ahead. But what’s surprising is that Windows 8 mobile is actually a very usable operating system that users should be able to become familiar with through the use of Windows 8 on laptops and desktops. Windows 8 gives users the added dimension of touch screen capabilities across the laptop, and desktop. Making the user experience more superior as it offers a third input alternative. After all, the more control a user has over the device, the higher the quality of the user experience.

Conclusion

Dell reported a pretty tough quarter as its net margins have declined while also losing market share to Apple Inc. (NASDAQ:AAPL). Increasing consumer adoption of Windows 8 brought by a product refresh cycle may increase the demand for Windows based computers.

Investors wanting a safer alternative should consider investing into Apple. Apple Inc. (NASDAQ:AAPL) offers a dividend yielding 2.84% plus it trades at a very reasonable 10.4 earnings multiple. Analysts on a consensus basis anticipate Dell to grow earnings by 9.67% per year over the next 5-years versus the growth that is projected for Apple at 20.88% per year for the next 5 years.

It seems like the clear winner is Apple Inc. (NASDAQ:AAPL).

The article Dell May Not Be Bought Out, So Buy Apple! originally appeared on Fool.com and is written by Alexander Cho.

Alexander is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.