Success is not guaranteed, but it seems likely that there are enough drug candidates for each company to exit the current round of development with a winning record. A solid case can be made explaining why each company is the best biotech company. Still, investors should refrain from trying to pick the best one. The group is so close at this early stage that attempting to label one better than the other would be an unproductive exercise and could even leave you with sub-optimal returns. History agrees.

We’ve seen this before

Investors should be wondering if shares are currently priced for perfection. It is a valid concern any time prices increase in a near-vertical manner. Some analysts believe pullbacks are inevitable. Others justify current share prices by looking to future earnings potential; earnings per share are expected to at least double across the board in the next few years.

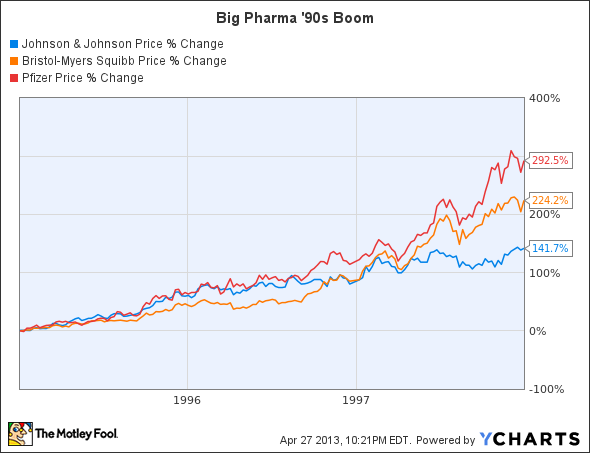

The run-ups above look surprisingly similar to those of big pharma in the mid-1990s in anticipation of major drug approvals. In fact, the pharmaceutical industry has yet to match the record two-year span of 1996 and 1997 that saw 100 drugs gain regulatory approval (a major reason for the patent cliff).

The good news is that the drugs behind the run-up were fueled by legends such as Lipitor, Plavix, Zyprexa, and Levaquin (and a few that never made it). This could serve as justification by those who support the current multiples of high-growth biotech stocks. The bad news is that most big pharma companies have yet to return to the all-time highs set during the mid-90s run-up — with just a few exceptions — even once drugs launched.

Be an investor, not a stock picker

If you’d invested $1,000 in one of the big pharma companies above on January 1, 1996 — at a time when each was considered a solid growth company — your returns would have varied wildly just eight years later on January 1, 2004:

| Company | Value of original $1,000 investment |

|---|---|

| Johnson & Johnson | $5,579 |

| Bristol-Myers Squibb | $3,792 |

| Pfizer | $2,060 |

Source: YCharts.

Conversely, if you had invested $333 in each company, you would be left with $3,810 — better than two of the alternatives!

One major reason to diversify pharmaceutical investments is not just to capture success, but to mitigate failure. Regulatory failures, market launch hiccups, slower-than-expected adoption, and market penetration will occur across the dozens of late-stage trials under way. Let’s not forget faulty mergers, acquisitions, and other corporate mistakes. Luckily for investors, Celgene Corporation (NASDAQ:CELG), Biogen, and Gilead have all enjoyed early successes. Just don’t get too comfortable.

Acing the first tests

Recently approved drugs with blockbuster potential will be the first tests for the high-growth biotech bunch, although all seem to have the winds at their backs initially. Celgene Corporation (NASDAQ:CELG)’s Pomalyst was approved as a third-line treatment for multiple myeloma in February. The drug should get a boost over Onyx‘s injectable Kyprolis for being orally administered and easily capture a chunk of the $6.5 billion multiple myeloma market, which is expected to double by 2017. Analysts believe the initial approved indication will be worth $1 billion in annual sales.

Biogen Idec Inc. (NASDAQ:BIIB) received approval for multiple sclerosis pill Tecfidera in late March. Fellow Fool Keith Speights believes it won’t have a problem ripping market share away from current therapies offered by Novartis and Sanofi thanks to a squeaky clean safety profile. Consensus forecasts call for the drug to hit $2.6 billion in sales by 2016 and nearly $4 billion by 2019.

Not to be outdone by its peers, Gilead Sciences, Inc. (NASDAQ:GILD) has received a string of approvals dating back to last August when its 4-in-1 HIV pill Stribild got the nod from the Food and Drug Administration. The drug is expected to rake in close to $5 billion in peak sales, according to Deutsche Bank, although the revenue stream will likely offset declining sales from aging therapies currently offered by Gilead Sciences, Inc. (NASDAQ:GILD). The company still has plenty to look forward to, especially with a recently submitted application for its newest hepatitis C pill, sofosbuvir. The all-oral therapy would be a first for the market, which is expected to reach $20 billion before the end of the decade.

Foolish bottom line

Celgene Corporation (NASDAQ:CELG), Biogen Idec Inc. (NASDAQ:BIIB), and Gilead Sciences, Inc. (NASDAQ:GILD) could all see earnings per share more than double in the next few years if leading drug candidates gain approval and enjoy a successful launch. But with failures imminent, why try to pick just one? Investors should instead consider spreading the risk and reward across the group. Would you rather gamble trying to choose the best biotech company, or check your ego at the door and own three great growth stocks (poor you)? If you weigh the risk and reward equally, the answer should be obvious.

The article Don’t Try to Pick the Best Biotech Company originally appeared on Fool.com and is written by Maxx Chatsko.

Fool contributor Maxx Chatsko has no position in any stocks mentioned. Check out his personal portfolio, his CAPS page, or follow him on Twitter @BlacknGoldFool to keep up with his writing on energy, bioprocessing, and emerging technologies.The Motley Fool recommends Celgene and Gilead Sciences.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.