From Momentum to Value Stock

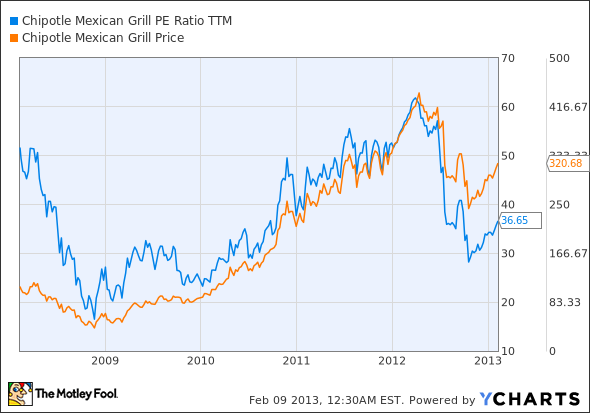

Throughout most its publicly traded life, Chipotle was considered a major momentum stock. To understand how hot Chipotle once was, we should compare its trailing P/E over the past five years, in comparison to its stock price.

CMG PE Ratio TTM data by YCharts

In early 2012, Chipotle’s P/E soared above 60 as its price surged into the $440s, completely outpacing the growth of its industry peers.

However, as P/E rises, market expectations grow until the company is unable to surpass estimates. That’s when fundamental gravity catches up and reconciles its price with its P/E multiple.

Therefore, Chipotle’s 27% plunge over the past year can be considered a rebalancing towards a more sustainable multiple. Let’s see how Chipotle stacks up fundamentally against its fast food rivals.

| Forward P/E | 5-year PEG | Price to Sales | Price to Book | Debt to Equity | Return on Equity (ttm) | |

| Chipotle | 31.26 | 1.81 | 3.63 | 7.95 | 0.28 | 24.28% |

| McDonalds | 14.89 | 1.88 | 3.45 | 6.84 | 95.53 | 38.66% |

| Jack in the Box | 15.22 | 1.44 | 3.16 | 0.82 | 102.25 | 15.40% |

| Yum Brands | 17.41 | 1.72 | 2.1 | 13.31 | 127.25 | 76.06% |

| Advantage | McDonalds | Jack in the Box | Yum | Jack in the Box | Chipotle | Yum |

Source: Yahoo Finance

Chipotle appears to be more expensive in every multiple and percentage, except for a key one – debt. Chipotle’s low debt shows that the company is spending and expanding responsibly, with strong financial controls.

For a more accurate picture of growth, we should also study how Chipotle’s EPS and revenue growth measures up to these rivals, and if it justifies these higher multiples.

CMG Revenue & EPS Diluted TTM data by YCharts

From these charts, it’s easy to see why growth investors have been enamored with the stock. But can it maintain that fantastic top and bottom line growth, or has growth finally peaked?

Future Growth

While Chipotle still has room to expand in the U.S. market and abroad, its growth may not come as easily as it did in the past.

Taco Bell’s Cantina Menu, which emulates Chipotle’s style of “gourmet bistro” fast food, is evolving into a serious competitor. Taco Bell’s 5,800 locations also form a much stronger distribution network that Chipotle’s 1,200 stores.

Meanwhile, Panera Bread’s reputation of “healthy” fast food could also slow Chipotle’s growth. Bistro fast food restaurants such as Panera have jumped into the niche market that Chipotle helped create, emerging as direct, domestic competitors rather than indirect, multinational ones such as McDonald’s, Starbucks or Yum.

Bottom Line

Chipotle is a fantastic growth stock that appears to be trading at a decent multiple. However, it is still a restaurant stock, and will be heavily exposed to macro factors such as food inflation and unstable commodity costs. The company’s lack of a value menu or diverse beverages could cause rigidity if those rising costs squeeze margins. The stock is not cheap – growth stocks rarely are – so it is not recommended for conservative value investors. However, its domestic and international growth – still in its infancy – is very appealing, and could lead to returns far exceeding its more mature industry peers.

The article Can Chipotle Still Serve Up Spicy Growth in 2013? originally appeared on Fool.com and is written by Leo Sun.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.