How many of us as investors want to identify companies that are pioneers in their industry? Is it possible to find commonality across sectors, which factors make specific companies great and cause other companies to fail?

A technology company like Oracle Corporation (NASDAQ:ORCL), which despite its tremendous size, continues to innovate and deliver value for shareholders by making smart bolt-on acquisitions. Or consider multimedia and entertainment giant The Walt Disney Company (NYSE:DIS), led by the visionary CEO Bob Iger, which is becoming the only game in town for digital content. Disney’s valuable ABC Television and ESPN lines are unequaled and generate more than half of the company’s profit for shareholders. And while many may not like Amazon.com, Inc. (NASDAQ:AMZN) as a company for understandable reasons, the stock has consistently performed well because Amazon is able to undercut competition and provide the lowest prices to its customers (Reference my articles on The Walt Disney Company and Amazon.com).

Each of these companies has at least one factor in common: a sustainable competitive advantage.

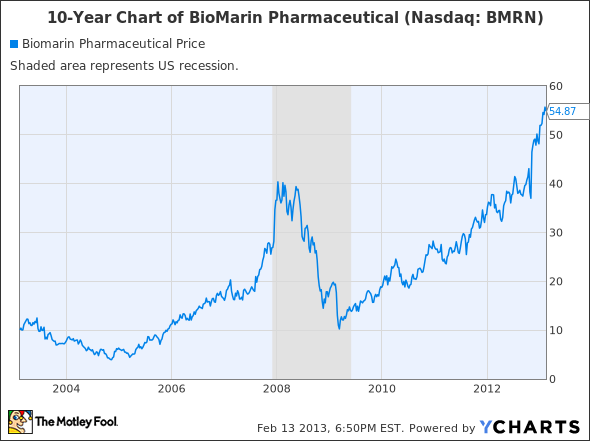

Let’s apply the same principle of competitive advantage to a market sector that investors often stray away from: the pharmaceutical industry. Consider the case of BioMarin Pharmaceutical Inc. (NASDAQ:BMRN), which reached an all-time high of $56.71 on Feb. 1. The company develops treatments for rare diseases and owns the rights to four market-leading drugs, three of which are the only FDA-approved medications in their respective categories.

BioMarin Pharmaceutical has risen 14% year-to-date and 51% in the last 12 months. In light of the stock’s recent run, here are four reasons I believe this breakout stock is headed significantly higher:

- The company expects to file for GALNS approval with the Food and Drug Administration no later than the end of March. GALNS is an acronym for galactosamine, an enzyme replacement therapy used to treat a rare disorder with no currently approved treatment. Approval in March could double the company’s annual sales from $500 million to $1 billion.

- Reuters recently reported that BioMarin has been approached by potential suitors interested in purchasing the company for a 25%-30% premium. CEO Jacques Bienaime acknowledged his company is indeed a target, saying a sale would come from the largest shareholders’ approval and not his own.

- In December, RBC Capital told investors that it sees a “50%+ chance” that BioMarin will be acquired in the next several years, given the company has one of the best drug pipelines among mid-cap biotech companies.

- On Jan. 21, Stifel Nicolaus upgraded BioMarin to Buy from Hold with a $67 price target, nearly 20% upside from Feb. 15’s closing price. Stifel Nicolaus believes that BioMarin’s product pipeline may produce better-than-expected results during fiscal 2013, and agrees the company makes an attractive acquisition target.

BioMarin gives notable mention on its investor relations website that it has brought three drugs to market in a 12-year period — an incredible feat for any company in the pharmaceutical industry. The company’s fourth listed drug, Firdapse, is only approved in the European Union and has yet to receive FDA approval.

The mean (average) price target on BioMarin is $58.11, while the highest target on Wall Street currently stands at $70.

A Speculative Play in Rare Diseases

Perceptive readers may note that BioMarin Pharmaceuticals isn’t the only company in the pharmaceutical industry that is dedicated to rare diseases. Sarepta Therapeutics Inc (NASDAQ:SRPT) is a development stage company that appears to have a breakthrough treatment called eteplirsen for the treatment of Duchenne’s Muscular Dystrophy (DMD).

BioMarin is also developing a treatment for DMD, although its compound BMN 195, a small-molecule utrophin upregulator, entered Phase I trials as recently as January 2010 with only a single patient. In contrast, Sarepta Therapeutics has completed both Phase I and II trials, and is planning to meet with the FDA to seek early approval following unprecedented success in its own clinical program.

In addition to rare diseases, Sarepta is developing treatments for infectious diseases such as ebola virus, influenza, and dengue fever. The stock has been extremely volatile since the company released positive Phase II results on Oct. 3, sending shares from $15 to $45 in a single trading session. Short sellers who question the data have brought the stock beneath $30, and Sarepta has been in a trading range between the low-to-high $20 range ever since.

In my opinion, the “easy money” in Sarepta is over. Depending on the company’s outcome with regulators, the stock is either worth $60 per share or a fraction of the current market price. Sarepta is also an attractive takeover target, whether the company receives immediate approval or otherwise. If regulators require Sarepta to complete further testing on eteplirsen, it’s possible management could choose to sell out.

Foolish Bottom Line

Analysts often compare BioMarin’s success in rare diseases to that of Genzyme early in its life cycle. Genzyme earned FDA approval for Cerezyme, used to treat Gaucher disease, and Fabrazyme, used to treat Fabry disease before being purchased by Sanofi SA (ADR) (NYSE:SNY) for a respectable premium. Sanofi made an initial offer for Genzyme in August 2010 for $18.5 billion, which was rejected by Genzyme’s board. Sanofi came back in February 2011 and offered $20.1 billion, accepted by shareholders.

BioMarin and Genzyme are so similar that the companies formed a joint venture to market BioMarin’s first drug Aldurazyme, which is effective for only 3,000 people in the developed world. Genzyme continues to fire on all cylinders, although investors would be required to purchase Sanofi SA in order to gain exposure. Sanofi has its own risks, with major patent expirations through mid-2013 and an uncertain pipeline. The company recently stated it expects flat to negative EPS growth for 2013.

For readers who dive into BioMarin’s financial statements, I would advise you not read into the company’s weak profitability in recent years. The company has been investing all of its cash into research and development, which is well-recognized by the Wall Street community. Furthermore, the stock trades completely on revenue expectations and its patent-protected pipeline.

As my friend Guy Adami states, “where there’s smoke, there’s fire” and a BioMarin sell-out seems nearly inevitable in a world where Big Pharma is searching for new drugs to fill an ever-widening patent expiration gap. I expect shares of BioMarin Pharmaceutical to be significantly higher in the next 12 months.

Thanks for reading, and consider subscribing to my posts for more Fool ideas on outperforming the market. Requests for future articles may be submitted to fool@johnmacris.com.

Investors interested in further reading in the biopharmaceutical space should reference Revlimid Ramp-Up, New Drug Launches Make Celgene a Buy. Shares of Celgene have risen approximately 26.4% between Nov. 28 and Feb. 15.

The article This Mid-Cap Pharmaceutical is a Prime Takeover Target originally appeared on Fool.com and is written by John Macris.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.