Apple Inc. (NASDAQ:AAPL)’s share price plunged 12% to $450 after posting an 18% sales increase, its weakest in 14 quarters and reporting the slowest profit growth in almost a decade.

The company itself is poised for growth, just not the phenomenal growth it had over the past few years. Apple Inc. (NASDAQ:AAPL)’s price decline has made it an excellent buy opportunity. Now that the company is trading at attractive valuations, it the most attractive mobile device investment on the market today.

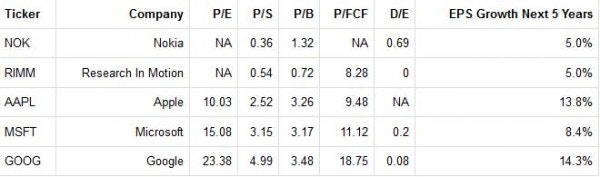

Putting Smartphone Growth and Value in Perspective

Apple Inc. (NASDAQ:AAPL) has the cheapest trailing earnings multiple of any profitable stock in the device space:

Apple Inc. (NASDAQ:AAPL) is clearly a better value than Google Inc (NASDAQ:GOOG) or Microsoft Corporation (NASDAQ:MSFT). It is trading at a price-to-earnings ratio that is lower than its peers and the market average. In addition, Apple trades at a solid price-to-free cash flow multiple and benefits from the most valuable brand on the planet. Yes, its price-to-sales multiple will probably fall as it lowers prices, but it will remain higher than industry and market averages based on consumer perceptions of brand value.

Nokia Struggling

Research In Motion, now Research In Motion Ltd (NASDAQ:BBRY), and Nokia Corporation (ADR) (NYSE:NOK) are speculative since neither one has made a net profit for the trailing twelve months. They are risky bets on the success of their new product launches.

Unfortunately, Nokia’s Lumia smartphones are not helping in the company’s bid to make a comeback in the U.S. It’s been the seventh straight drop in quarterly sales for the company. These desperate times marked the first time the company did not pay a dividend in nearly 150 years.

Tough competition from both Apple Inc. (NASDAQ:AAPL)‘s iPhone and smartphones that run on Google’s Android OS limited the sales of the Finland-based company to only 700,000 units during the fourth quarter. This is a significantly lower number than several analysts’ sales forecast of at least 1 million Lumias. Around the world, there were 4.4 million Lumias sold during the holiday quarter, just a fraction of the nearly 48 iPhones sold, or the gargantuan 136 million Android-running devices now on customer’s hands.

One of the reasons might be that the Lumia smartphones are trailing far behind their competitors in the number of applications available. As well, Nokia hasn’t been able to give their prospective buyers reasons to switch from Android or Apple handsets, as credit analyst at Danske Bank (DANSKE) Louis Landeman said , “Customers just don’t have a natural attraction to the name. The 700,000 unit sales in North America need to improve if Nokia is ever going to have a chance to boost its market share”.

Apple Already Ahead

Unlike its peers, Apple is already ahead in the smartphone game.

Fiscal first quarter income increased about 1% to $13.1 billion, equivalent to $13.81 per share. Sales for the same period grew 73% versus a year earlier. Although Chief Executive Officer Tim Cook steered Apple to record revenues through iPad and iPhone sales, investors are wary that management may not be able to sustain coming up with hit products more than a year after Steve Jobs’ death. The recent quarter results also fueled concerns that increased competition from Samsung Electronics and mounting costs amid a maturing smartphone will continue to curtail growth.

While Apple sold 12.7 million iPads during the quarter, beating projection for 11.4 million units, its revamped Mac personal computer sold only 4.1 million units, a million short of analysts’ estimates. Cook said Apple couldn’t churn out units fast enough to keep pace with strong demand, thus curbing sales.

Last year, Cook reinstated the company’s dividend, which was stopped since 1995. Until Apple starts giving more of its $137.1 billion cash pile to investors it won’t truly become a value stock. The company’s 2.4% dividend yield is still behind similar technology companies like Intel Corporation (NASDAQ:INTC) which pays out 4.3%, Hewlett-Packard Company (NYSE:HPQ) with 3.1% and Microsoft Corporation (NASDAQ:MSFT) whose indicated yield is 3.3%. Chief Financial Officer Peter Oppenheimer told analysts that last quarter, Apple paid out about $4.5 billion in cash between dividends and stock buyback and plans to increase both.

Weak Investor Sentiment is a Buying Opportunity

BTIG co-head of research Walter Piecyk said , “People are concerned about how quickly sales are falling off after the initial product launches and whether the company can deliver new and interesting products to reignite growth.”

Apple’s price decline is not just a result of portfolio rebalancing, but a lack of faith in Apple’s products, as could be seen by declines in Apple supplier stocks. The shares of Apple suppliers were somewhat down with Hon Hai Precision Industry, its assembler, dropping 2.9% in Taiwan; AAC Technologies Holding, speaker-maker, down by 6% in Hong Kong and chip-maker Samsung falling 1.4% in Seoul. In New York, circuit-maker Cirrus Logic plunged 11% to $26 while flash memory supplier Fusion-io shed 1.1% to $21.

To address investors’ concerns over decreasing market share, Cook said Apple gives consumers more options and continues to sell older models at reduced prices, such as the iPhone 4 which was still selling out during the quarter. In China, where the company opened 4 stores in the past quarter, sales grew 67% to $6.8 billion.

With the latest results, analysts are now inclined to look at Apple as a value stock. After years of spectacular growth, they predict the new trend will continue and Apple will be like AT&T Inc. (NYSE:T) or International Business Machines Corp. (NYSE:IBM), offering investors more predictable earnings and steady dividends corresponding to slower sales growth. Mizuho Securities analyst Abhey Lamba said , “This is a big shift in the company’s position from a year ago. The growth has slowed down much faster than we anticipated.” Other analysts agree and think that Apple may soon attract value investors in view of these latest reports.

Some investors however, see Apple will regain growth ahead. The company earned $13.1 billion profit out of $54.5 billion sales for the first quarter and revenue would have been higher if supply constraints had not prevented it from keeping up with demand. Wedgewood Partners chief investment officer David Rolfe said , “This is not by any stretch of the imagination a broken company.”

Conclusion

The smartphone market is going to see lower prices for devices and lower profits. While future rivalry and price reductions are already priced into Apple shares, they still present an excellent buying opportunity for investors looking at the tech sector.

The article Apple’s Growth Slows, But Still An Attractive Buy originally appeared on Fool.com and is written by Bill Edson.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.