The biggest increase in value comes from increasing the margin, accounting for a little bit more than half of the value change, followed by higher revenue growth and then by lower costs of capital. Note that the firm’s debt load magnifies the effects of changes in the value of operating assets on equity value, and the options that had dropped in value with the stock price in June 2019, are reasserting their role as a drain on value. If there is a lesson that I would take away from this table, it is that the key debate that we should be having on Tesla is not about whether it can grow. Given the size of the auto market, and the shift towards electric cars, the growth is both possible and plausible. It is about the margins that Tesla can command, once it becomes a mature company, which in turn requires an assessment of what the auto market will look like a decade from now. If you believe that an electric car is an automobile first, and electric next, it will be difficult to reach and sustain double-digit operating margins, if you are not a niche auto company. If, in contrast, your view is that the electric car market will be viewed as an electronic or tech product, you may be able to justify higher margins.

What now?

In the interests of transparency, I should start with a confession. I went into this valuation wanting to hold on to Tesla for a little while longer, partly because it has done so well for me (and it tough to let winners go, when they are still winning) but mostly because at a 7-month holding period, selling it now will expose me to a fairly hefty tax liability; short-term capital gains (less than a one-year holding period) are taxed at my ordinary tax rate and long term capital gains (greater than a year holding period) are taxed at a 20% lower rate. This desire to derive a higher value for Tesla (to justify continuing to hold it) may be driving the optimism in my assumptions in the last section, but even with those optimistic assumptions, my value per share of $427 was well below the closing price of $581 at the end of trading and even further below the $650 that Tesla was trading at after the earnings release.

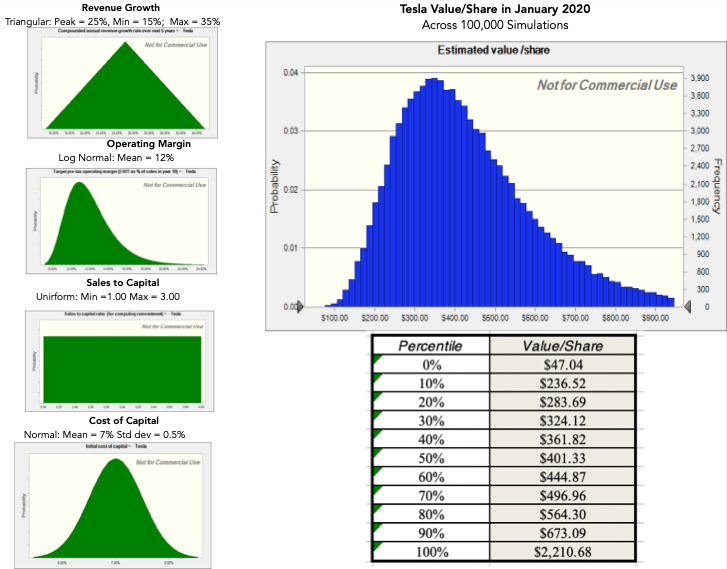

Could tweaking the assumptions give me a value higher than the price? Of course! I could raise my end year revenues to $200 billion ( plausible in a market this size) and give Tesla an 18% operating margin (perhaps by calling it a tech company) and arrive at a value of $ 1,168 per share, but that to me is pushing the limits of possibility, and one reason why I hold back on simple what-if analyses. A Monte Carlo simulation allows for a more complete assessment of uncertainty and in the table below, I vary four key assumptions (revenue growth, target margin, reinvestment efficiency and cost of capital) to arrive at a value distribution for Tesla:

|

| Simulation Results |

At the price of $650/share, post-earnings report, Tesla is close to the 90th percentile of my value distribution. While it possible that Tesla could be worth more than $650, it is neither plausible nor probable, at least based on my assumptions.