A Personal Viewpoint

I have been skeptical about both the reasons given for active investing’s slide over the last decade and the dire consequences of passive investing, and this crisis has only reinforced that skepticism. For active investing to deal with its very real problems, it has to get past denial (that there is a problem), delusion (that active investing is actually working, based upon anecdotal evidence) and blame (that it is all someone else’s fault). Coming out of this crisis, I think that more money will leave active investing and flow into passive investing, that active investing will continue to shrink as a business, but that there will be a subset of active investing that survives and prospers. I don’t believe that artificial intelligence and big data will rescue active investing, since any investment strategies built purely around numbers and mechanics will be quickly replicated and imitated. Instead, the future will belong to multidisciplinary money managers, who have well thought-out and deeply held investment philosophies, but are willing to learn and quickly adapt investment strategies to reflect market realities.

Small versus Large Cap

The small cap premium was among the earliest anomalies uncovered by researchers in the 1970s and it came from the recognition that small market capitalization stocks earned higher returns than the rest of the market, after adjusting for risk. That premium has become part of financial practice, driving some investors to allocate disproportionate portions of their portfolios to small cap funds and appraisers to add small cap premiums to discount rates, when valuing small companies.

The Difference

There are two things worth noting at the outset about the small cap premiums. The first is that market capitalization is the proxy for size in the small cap studio, not revenues or earnings. Thus, you can have a young company with little or no revenues and large losses with a large market capitalization and a mature company with large revenues and a small market capitalization. The second is that to define a small capitalization stock, you have to think in relative terms, by comparing market capitalizations across companies. In fact, much of the relevant research on small cap stocks has been based on breaking companies down by market capitalization into deciles and looking at returns on each decile. One reason that the small cap premium resonates so strongly with investors is because it seems to make intuitive sense, since it seems reasonable that small companies, with less sustainable business models, less access to capital and greater key person risk, should be riskier than larger companies.

The Lead In

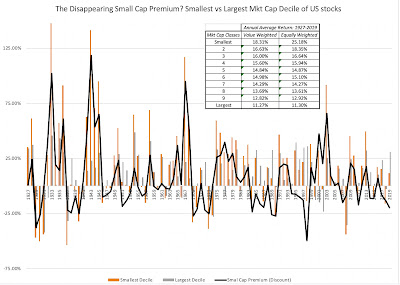

As with value investing, the strongest arguments for the small cap premium come from looking at historical returns on US stocks, broken down by decile, into market cap classes.

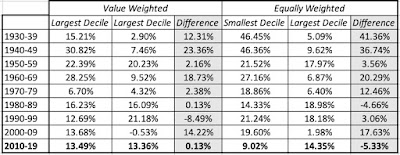

Going back to 1927, the smallest cap stocks have delivered about 3.47% more annually than than the rest of the market, on a value-weighted basis. That outperformance though obscures a troubling trend in the data, which is that the small cap premium has disappeared since 1980; small cap stocks have earned about 0.10% less than the average stock between 1980 and 2019. The table below breaks down the small cap premium, by decade:

The data in this table is testimony to two phenomena. The first is the belief in mean reversion that lies at the heart of so many investment strategies, with the mean being computed over long time periods, and primarily with US stocks. The second is that once bad valuation practices, once embedded in the status quo, are very difficult to remove. In my view, the use of small cap premiums in valuation practice have no basis in the data, but that does not mean that people will stop using them.

The Crisis Performance

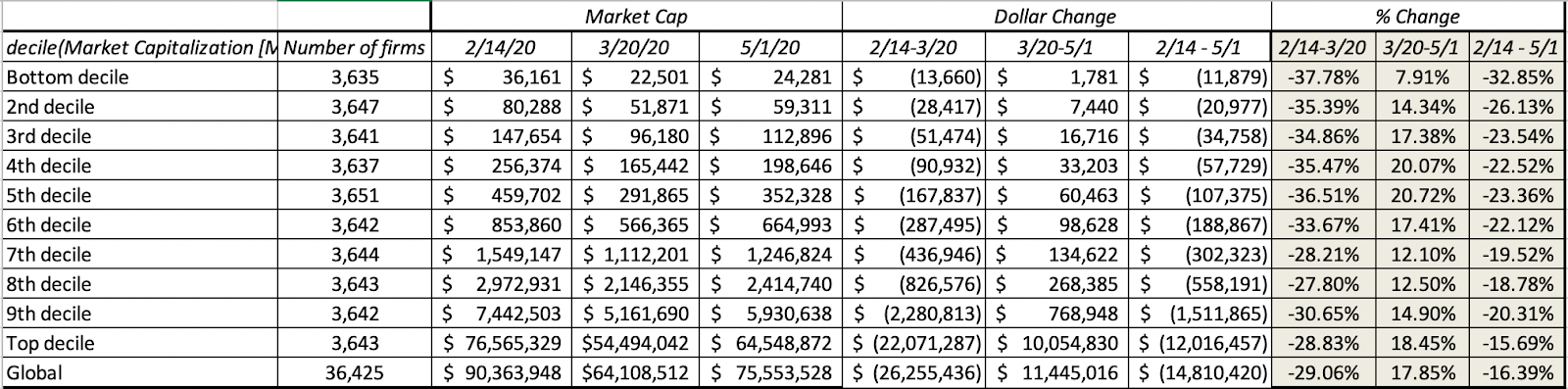

As with active and value investing, there are some who believe that the fading of the small cap premium is temporary and that it will return, when markets change. To the extent that this crisis may constitute a market shift, I examined the performance of stocks, broken down by market capitalization into deciles between February 14, 2020 and May 1, 2020.

I know that it is still early in this crisis, but looking at the numbers so far, there is little good news for small cap investors, with stocks in the lowest two declines suffering more than the rest of the market. In fact, if there is a message in these returns, it is that the post-COVID economy will be tilted even more in favor of large companies, at the expense of small ones, as other businesses follow the tech model of concentrated market power.