Another Tibco Software Inc. (NASDAQ:TIBX) earnings report and it’s another miss, another guidance downgrade and another series of expressions of dissatisfaction with its own salesforce. As such, the stock now appears to be at a crucial juncture whereby its guidance is so low that rectifying the execution problems could lead to a significant earnings beat and a rapid recovery. Alternatively these misses could be representative of a market that is structurally changing against Tibco Software Inc. (NASDAQ:TIBX). In this article I’m going to outline what the management has been saying over the last year.

Tibco’s Miserable Year

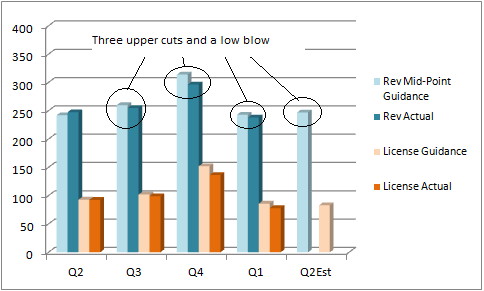

The story of TIBCO’s performance over the last year is personified in the following chart:

In short it’s been a pretty miserable year for investors, and the failure to beat internal guidance is even worse.

In order to demonstrate this I have compared the midpoint of the previous quarter’s guidance with what actually happened.

Now let’s recall that this guidance has been given at a time when the company would have already been through the larger part of a month within the three month period. Of course this is why stocks react so negatively to earnings misses. As Jack Welch famously pointed out, companies should do everything they can to avoid missing them. A company that continues to miss its own guidance will do damage to its market credibility.

What TIBCO Said

I’m going to run through a summation of the earnings calls this year and what management said on them.

Q1 2012- CEO & President Vivek Ranadive remarked that TIBCO had never seen ‘such pricing power.’ When asked about competitive pressures from its chief middleware competitors International Business Machines Corp (NYSE:IBM) and Oracle Corporation (NASDAQ:ORCL) and specifically if they were bundling middleware in order to undercut TIBCO, Ranadive answered that IBM was its main rival but that he felt ‘very comfortable’ with TIBCO’s competitive position. Later on in the same call SAP AG (ADR) (NYSE:SAP) and Oracle were described as ‘dinosaurs’ competing with old fashioned technology.

Q2 2012- This quarter saw some relatively better numbers, and Tibco Software Inc. (NASDAQ:TIBX) was described as operating under the ‘best of times’ by Ranadive.

However, the guidance wasn’t great, and the problem of US sales execution was cited. The regional trends for Tibco Software Inc. (NASDAQ:TIBX) can be seen in this graph.

When asked about the timing of a turnaround in US prospects, management replied that what they were seeing right now ’is opportunity’ which needed investing in. Later on Ranadive declared that he was ‘very, very confident’ that TIBCO would get back on track as early as the current quarter. The main adjustment was to have the North American sales people reporting directly into a senior level TIBCO VP Murat Sonmez.

Q3 2012- Roll on Q3 and a disappointing set of numbers, but that didn’t stop Tibco Software Inc. (NASDAQ:TIBX) from guiding towards some pretty good license sales growth in Q4. Indeed, Ranadive told analysts that the company was sitting on a $500 million pipeline. Deals were seen across all geographies and industries. Surely TIBCO would bounce back?

Q4 2012- I recall this conference call very well because I’ve rarely heard such a candid assessment of a company’s performance. Time and time again TIBCO pointed out that the problem wasn’t macro or product. It was execution, specifically with the US. The relatively better performance in Europe was cited to back this view up.

The pipeline previously discussed did not close as expected, and ’10 to 20’ deals slipped. Naturally Ranadive & co were grilled over the issue. He argued that some deals were lost thanks to ‘sloppiness’ and the deals that slipped were not lost but rather delayed. IBM was cited as its biggest competitor, but the problem was ‘absolutely an execution related’ issue in the US.

Raj Verma was appointed to oversee a turnaround in the US; he was supposed to bring an attention to detail and overall scrutiny that might help turn things around for TIBCO.

Q1 2013- Fast forward to the recent results and Europe is now weak, the US problems are ongoing, the guidance is horrible, and now there is a problem with the UK operations! TIBCO has had more execution problems than Robespierre, and I will leave the reader to look at the charts above to see how poor the guidance is for the next quarter.

Where Next for Tibco Software Inc. (NASDAQ:TIBX)?

Who knows? Overall the big data sector has done well this year with the only weakness being seen in something like Teradata Corporation (NYSE:TDC). Okay, Oracle reported some weak numbers recently, but then it had had a particularly strong quarter previously. Meanwhile, IBM’s last quarter was good and corporations (particularly US) don’t appear to have made significant cutbacks lately.

So if it isn’t macro then what is it? Everything that management is pointing at indicates that it’s internal execution, but this has been going on for nearly a year now and it seems to be infectious with Europe now catching a cold and the UK catching a fever. It’s hard not to conclude that this isn’t at least partly an erosion of competitive positioning–the suspect will be IBM.

In conclusion Tibco Software Inc. (NASDAQ:TIBX) has much to do to regain investor’s confidence. It is no doubt an attractive recovery proposition right now, but it is certainly not a stock for those of a nervous disposition or for those who only buy stocks where the management has got its guidance accurate in recent quarters. Perhaps TIBCO should use some of its own big data analytics on itself when it sets guidance?

The article A Look Back at TIBCO ‘s Guidance to Investors originally appeared on Fool.com and is written by Lee Samaha.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.